RZH News: Spencer Cooper Named As AdvisorHub’s Advisor to Watch

We are pleased to share that Spencer Cooper, Principal and Chief Wealth Strategist at RZH Advisors, has been named to AdvisorHub’s 2026 Advisors to Watch: RIAs list. This list recognizes 1,000 Registered Investment Advisors from across the country who have demonstrated excellence in practice management, growth, and professionalism.

Those who know Spencer understand that this recognition reflects the same qualities he brings to every client relationship – thoughtful guidance, genuine care, and a commitment to helping individuals and families make confident financial decisions.

At RZH, we are fortunate to have Spencer as part of our team, and we are grateful for the trust you place in him and all of us as we help you navigate your financial journey.

Please join us in congratulating Spencer on this well-deserved recognition.

To learn more about important ranking methodology, please click HERE.

AdvisorHub’s 2026 Advisors to Watch – RIAs ranking was published on June 16, 2026, and is based on data provided by participating advisors and firms. Rankings are determined using a proprietary methodology that considers factors such as assets under management, growth, client retention, practice quality, regulatory record, community involvement, and team diversity.

RZH Insights: Is Your Index fund Really “Passive”?

In last month’s edition of RZH Insights, Brendan McEwan walked us through the latest SPIVA® (S&P Indices Versus Active) U.S. Scorecard – a ledger of evidence showing that the vast majority of active fund managers have failed to beat their benchmarks over time.1 The data was striking: 79% of active large-cap U.S. equity funds underperformed the S&P 500 Index in 2025 on an absolute basis, and over a 15-year horizon, the numbers climbed to nearly 90%.2

These results beg the question: What is it about the S&P 500 Index that makes it so difficult to beat?

The S&P 500, and the investment vehicles that track it, are commonly labeled as “passive” investments, suggesting a static list of 500 companies, assembled mechanically, requiring no human judgment. That assumption could not be further from the truth, and a look under the hood reveals a highly dynamic index that, as we will soon see, is built on the same principles that underpin RZH’s approach to long-term investing.

Behind the Curtain: How the S&P 500 Is Actually Built

The S&P 500 is not simply the 500 largest companies in the United States. It is a curated index, selected and maintained by a committee of analysts and economists at S&P Dow Jones Indices who meet monthly and exercise real discretion over its composition.3

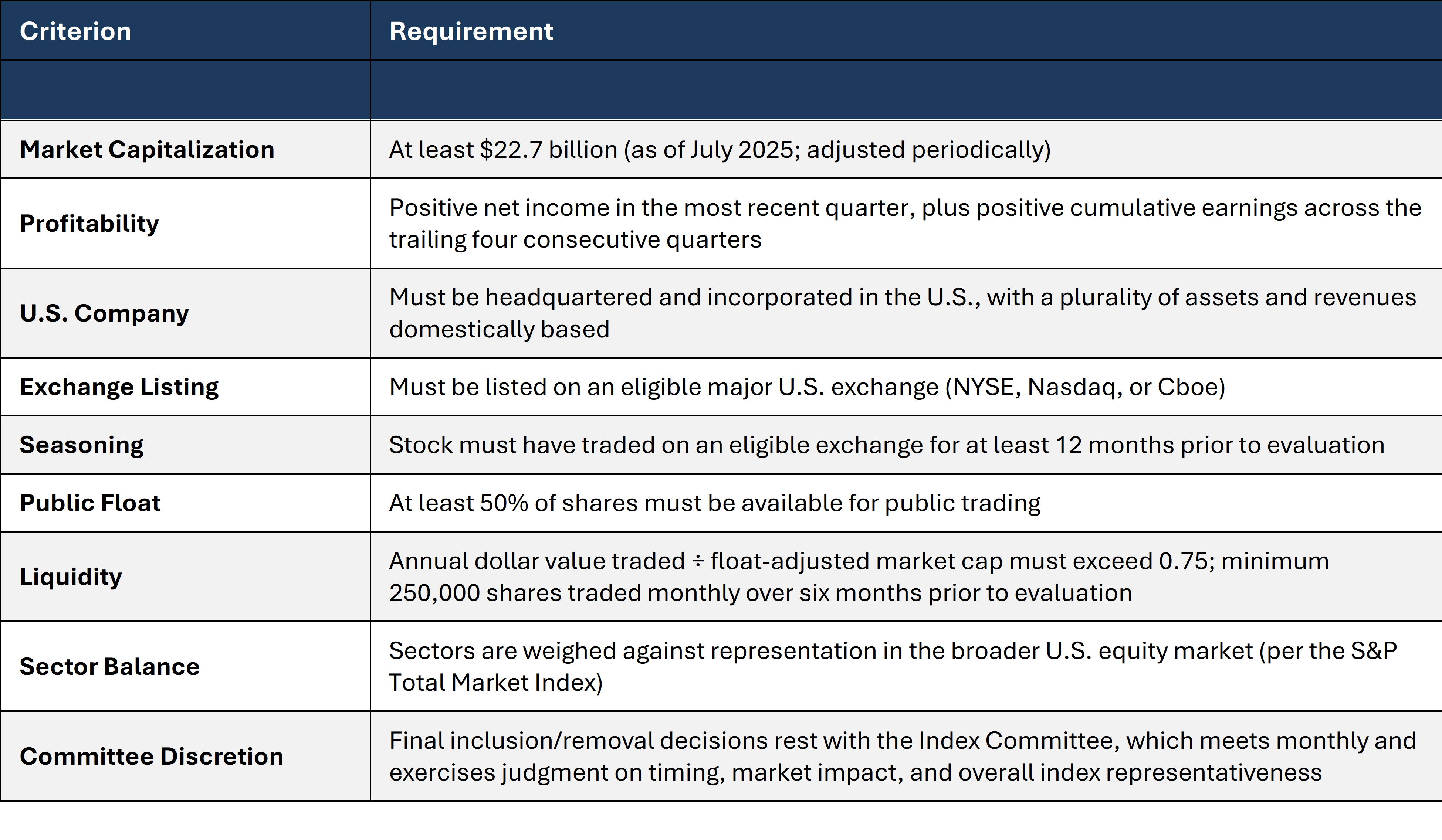

To even be considered for inclusion, a company must clear several hurdles: a minimum market capitalization of $22.7 billion (as of July 2025), positive GAAP net income from continuing operations in the most recent fiscal quarter (and positive total net income over the four most recent quarters), minimum trading volume and liquidity requirements, and a sufficient public float.4 In other words, the Committee imposes a rigorous screen on size, quality, liquidity, and investability to determine the universe of companies eligible for inclusion, prioritizing large and liquid stocks with persistent earnings and weeding out thinly traded ones and those with sporadic or financially engineered profits. But meeting those criteria does not guarantee a seat. The Committee weighs additional factors, most notably sector balance, comparing each sector’s representation in the index against its weight in the broader U.S. equity market.5 If technology stocks are overrepresented relative to the total market, the committee may pass over an otherwise-qualified tech company in favor of a candidate from an underweight sector. This is a critical distinction. As S&P Dow Jones Indices states in its own methodology: the index is not rules based and all changes are “fully discretionary and are determined by the Index Committee.”6 Contrast this with the Russell 1000, which is purely mechanical: a company either meets the size threshold or it doesn’t.7 The S&P 500 involves human judgment at every turn. Indeed, while definitionally “passive,” one of the most widely held investments in the world rests on a foundation of active decision-making.

S&P 500 Eligibility Criteria

Source: S&P Dow Jones Indices, S&P U.S. Indices Methodology, April 2026; Investopedia; S&P Global

Built to Evolve

The committee’s work doesn’t stop at selection. The index is continuously reconstituted – companies are added and removed in response to mergers, acquisitions, financial deterioration, and shifts in the economy. On average, roughly 20-30 companies are replaced each year.8 A Goldman Sachs analysis published in early 2026 found that since 1985, approximately 20% of S&P 500 constituents turn over every five years.

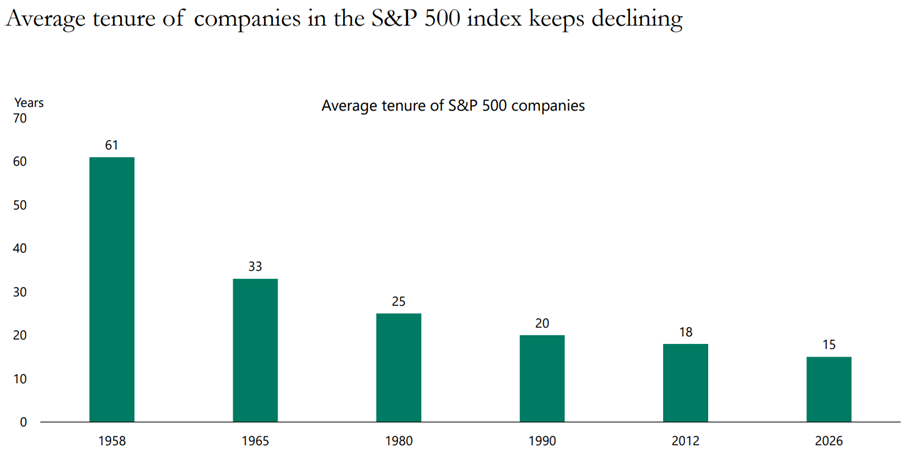

The result is an accelerating pace of creative destruction within the index itself. Research from Innosight found that the average tenure of a company on the S&P 500 has declined from 33 years in 1964 to roughly 15 years today – and is forecast to shrink further in the years ahead.10 At the current churn rate, approximately half of today’s S&P 500 constituents will be replaced over the next decade!11

Sources: Creative Destruction Whips Through Corporate America, Corporate Longevity: Turbulence Ahead for Large Organizations – Executive Briefing, 2021 Corporate Longevity Forecast | Innosight, Apollo Chief Economist

Let’s take another look at the index’s evolution, this time focusing on the leaders over the past 50 years:

Top 10 companies in the S&P 500 by market capitalization

Source: 1985–2025: J.P. Morgan Asset Management Guide to the Markets, 1Q 2026 | 1975: Historical research

In 1975, the ten largest companies in the S&P 500 included IBM, AT&T, Sears Roebuck, Eastman Kodak, and General Motors – titans of the industrial economy.12 By 2025, every one of those names had either been replaced, acquired, or restructured beyond recognition. Today’s top ten reflect a fundamentally different economy, one driven by technology, cloud computing, and artificial intelligence. The combined market capitalization of the top ten has grown from roughly $115 billion in 1975 to over $19 trillion in 2025.12

The index didn’t ask anyone to predict that shift. It simply rewarded the companies that earned their way to the top and removed the ones that didn’t. Old economy stocks were replaced by new economy leaders. The cap-weighted structure ensures that the most successful companies naturally receive the greatest weight, while those that falter shrink in influence and are eventually shown the door.

This is not a static basket of stocks. It is a living, self-correcting representation of American enterprise.

A Level(er) Playing Field

The index’s built-in quality controls help explain part of its dominance as a benchmark. But active management was already a difficult proposition well before the index became a household name.

As Howard Marks, cofounder of Oaktree Capital Management, observes, “on average, all investors will do average.” Active management, in other words, “constitutes a zero-sum game (or negative-sum after commissions and other costs).”13 To outperform, a manager must consistently identify moments when consensus pricing is wrong and act on that judgment correctly. As markets have grown more efficient, access to information has proliferated, and the pool of well-resourced, sophisticated participants (human and non-human) has expanded, the odds of doing so consistently have narrowed.

A regulatory shift in the early 2000s raised the bar further. Before October 2000, publicly traded companies routinely disclosed material information – earnings guidance, product developments, strategic concerns – selectively to institutional investors and analysts before sharing it with the broader public.14 This information asymmetry gave active managers a genuine, structural edge. The analyst who had a direct line to a company’s CFO simply had better information than the rest of the market.

The SEC’s Regulation Fair Disclosure (Reg FD), enacted in August 2000, changed this by requiring companies to disclose material nonpublic information to all investors simultaneously, leveling the playing field overnight.15 Research by Gintschel and Markov supports this intuition, finding that the average price impact of information disseminated by financial analysts dropped by 28% in the post-regulation period.16

What This Means for Your Plan

The lesson here is not that you should only own index funds. A sound plan extends well beyond U.S. large-cap equities; it incorporates global diversification and tailors the portfolio to your specific circumstances as dictated by your plan. Active strategies can and do serve important roles within a well-constructed portfolio, whether that means generating tax efficiencies, managing around concentrated stock positions, expressing personal values, or addressing any number of client-specific objectives that a broad index cannot. The question is not whether active management has value. It is whether the tools being used are serving a plan designed to achieve your most important financial goals.

The S&P 500 exemplifies a set of investment principles that, in our view, have generally been effective over long periods: own a diversified portfolio of high-quality companies, remain invested across market cycles, let the winners compound, prune what no longer works, rebalance with discipline, and remain patient.

These principles mirror those we employ in managing your wealth.

The companies at the top of the S&P 500 in 2045 will likely look different from today’s leaders -just as today’s leaders look nothing like those of 1975. That is not a flaw, but a feature of the system and a result of corporate innovation and the ability of successful companies to continue building, growing, and creating value over time. It means that neither the index, nor the plan built around it, depends on the permanence of any single company, any single sector, or any single chapter of the American economy. It depends on the enduring capacity of American enterprise to innovate, adapt, and grow – a resilience that has stood the test of time and will, in our view, continue to endure.

[11] The bar for removal from the index is intentionally higher than for inclusion. If a stock falls below the minimum threshold, it is not automatically removed; it stays “unless ongoing conditions warrant an index change” (S&P U.S. Indices Methodology). The Committee’s discretion also serves to dampen turnover due to temporary market or economic conditions. Consider AIG: the U.S. government’s bailout during the 2008 financial crisis left the Treasury owning over 90% of the company, technically violating the public float requirement, yet the committee chose not to remove it, as doing so would have amplified an already severe market panic. See Blitzer as quoted in “Passive-Aggressive? Behind the Curtain at S&P 500,” TheStreet; RBC Wealth Management, “A Closer Look at the S&P 500.”

[12] J.P. Morgan Asset Management, Guide to the Markets, 1Q 2026. Historical research for 1975 data. RZH Advisors.

[13] Marks, Howard. “I Beg to Differ.” Oaktree Capital Management Memo. See also Marks, Howard. The Most Important Thing: Uncommon Sense for the Thoughtful Investor. Columbia University Press, 2011.

[15] Ibid. SEC Press Release, August 15, 2000. ¹⁶ Gintschel, Andreas and Markov, Stanimir. “The Effectiveness of Regulation FD.” Journal of Accounting and Economics, 2004. See also Agarwal, V., et al., “The Effect of Regulation FD on Active Share and Fund Performance”; “Reg-FD and the Competitiveness of All-Star Analysts,” Journal of Accounting and Public Policy (2008).

RZH Insights – The Scorecard Never Lies: 25 Years of Proof That Indexing Wins

What the 2025 SPIVA Report tells us — and why, after a quarter century, the answer hasn’t changed.

Over the past year and roughly 2 weeks, U.S. equities have risen more than 45%1, while international markets are up over 41%2. RZH’s investment philosophy and disciplined approach have enabled our fully-invested clients to capture the majority – if not all – of this historic rally, once again reinforcing the value of our long-term strategy.

The benefits of this approach are further highlighted each year when S&P Dow Jones Indices publishes its SPIVA® (S&P Indices Versus Active) U.S. Scorecard — a detailed analysis of how actively managed funds fared against their benchmark indices. We have shared this data with you before, and we will continue to do so, because after 25 years it remains one of the most powerful and actionable truths in all of investing.

The year-end 2025 edition is in. And once again, the story is the same — only more so.

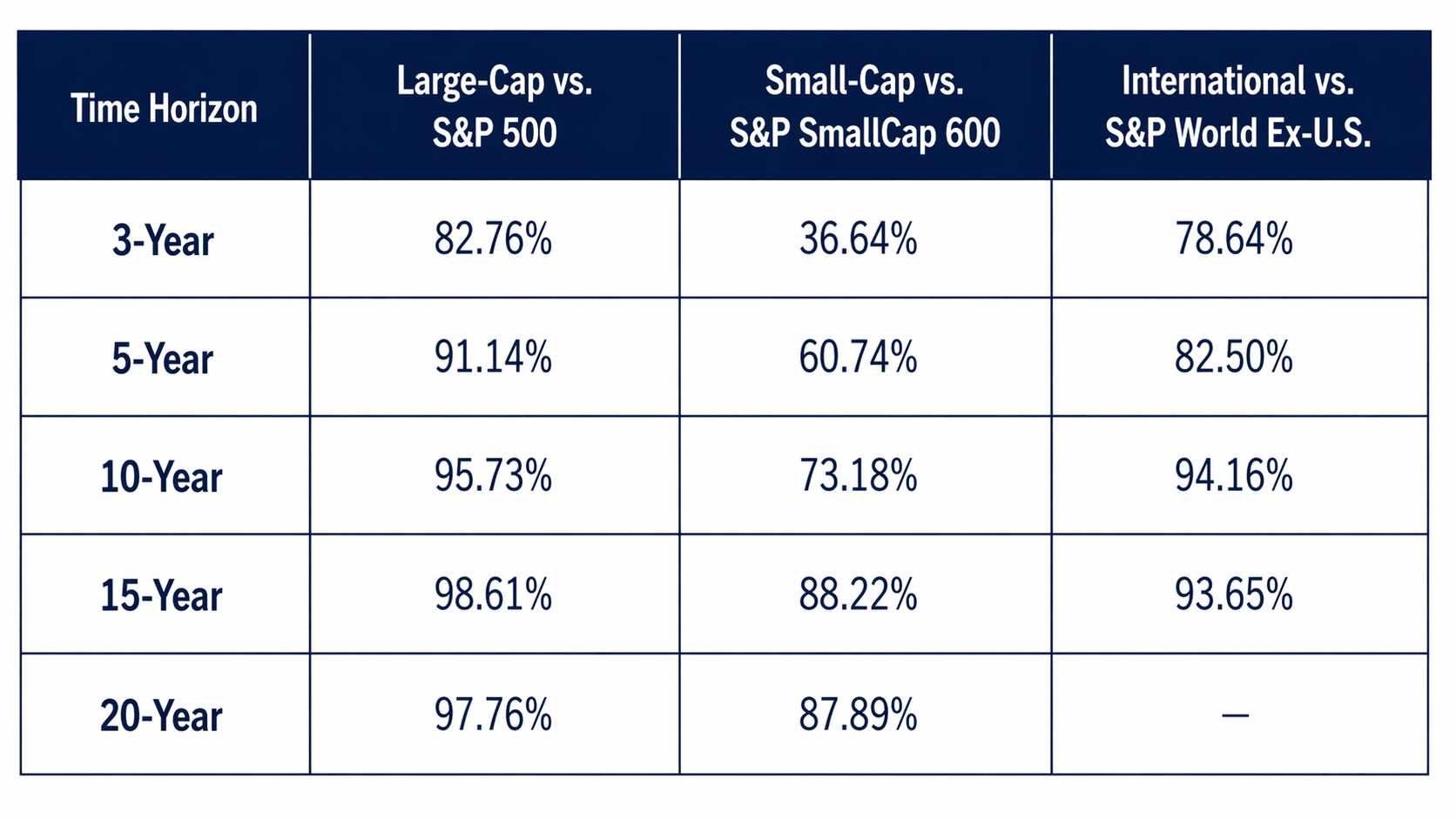

79% of all active large-cap U.S. equity funds underperformed the S&P 500 in 2025 — up sharply from 65% the year before, and the fourth-worst result in the scorecard’s history.3

Consider that for a moment: in a year when markets were volatile, when tariff fears briefly sent the S&P 500 into near-bear-market territory4, when stock-level dispersion reached its highest point since 20095 — in other words, in conditions that were supposedly ideal for skilled active managers — nearly four out of five still lost to the index.

There are a few nuances worth noting. Small-cap active managers had a relatively better year — “only” 41% underperformed, versus historical norms well above 60%.3 International managers also fared better than their large-cap U.S. counterparts, aided by strong non-U.S. performance and wider country-level dispersion. But here is the critical point: even in the “good” categories, a majority still failed to beat a simple index.

One Good Year Doesn’t Change a 25-Year Record3

Source: SPIVA® U.S. Scorecard, Year-End 2025, S&P Dow Jones Indices LLC, CRSP. Data as of December 31, 2025.

Whenever a category of active managers has a decent year — as small-cap managers did in 2025 — the temptation is to conclude that the case for active management is being rehabilitated. We’ve seen this movie before. The data over longer time horizons tells a very different story.

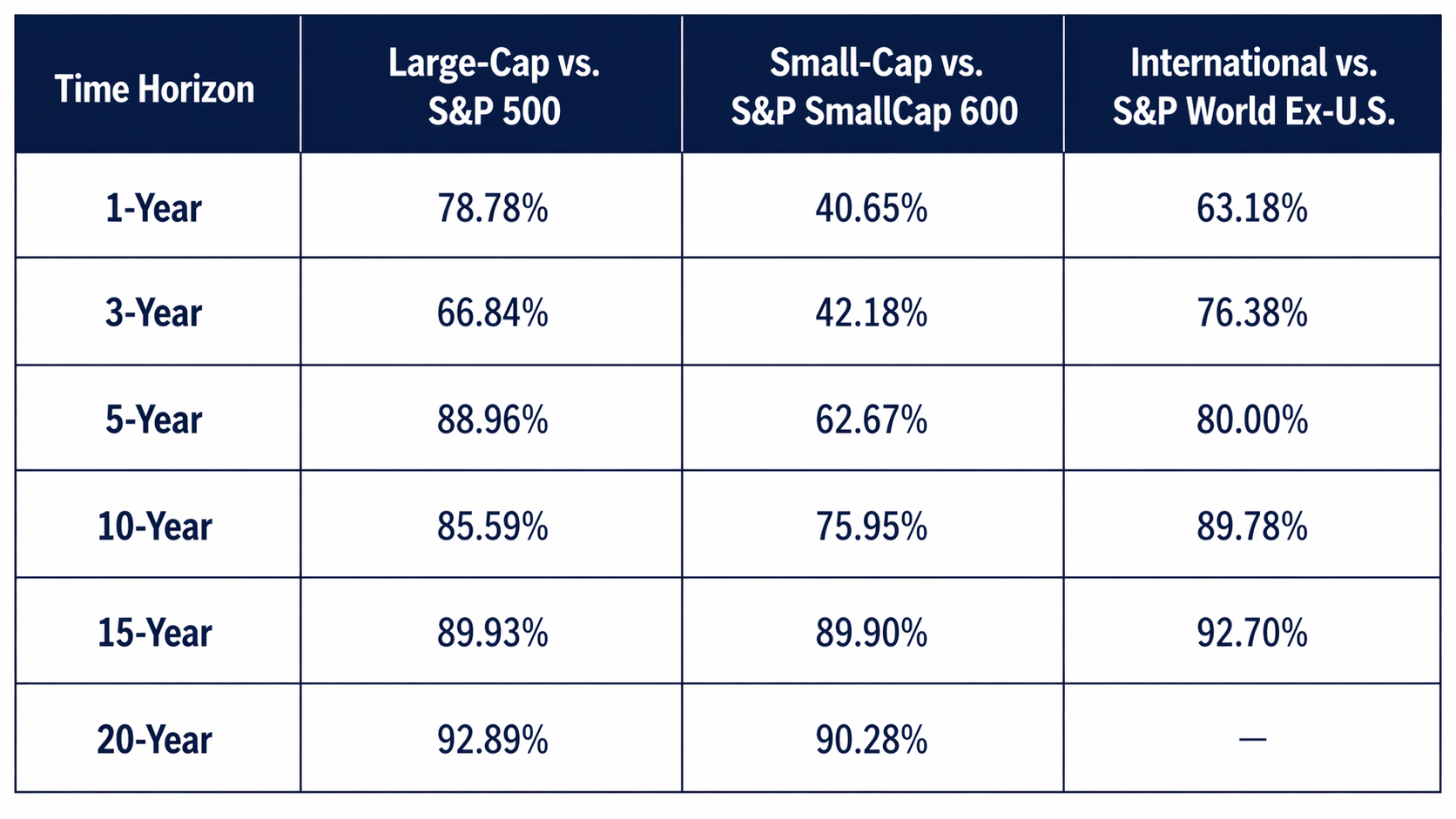

Below are the underperformance rates for active managers across large-cap, small-cap, and international categories over multiple time horizons:3

Table 1: % of Active Funds Underperforming Their Benchmark (Absolute Return)3

Table 2: % of Active Funds Underperforming Their Benchmark (Risk-Adjusted Return)3

Source: SPIVA® U.S. Scorecard, Year-End 2025. Large-Cap: Report 1a/1b vs. S&P 500. Small-Cap: Report 1a/1b vs. S&P SmallCap 600. International: Report 6a/6b vs. S&P World Ex-U.S. 20-year international risk-adjusted data not available. Past performance is no guarantee of future results.

The charts show that whether measured on an absolute or risk-adjusted basis, the pattern is the same across all three categories: the longer the time horizon, the worse active management looks. The risk-adjusted numbers are even more striking — by 15 years, nearly 99% of large-cap managers and over 88% of small-cap managers failed to beat their benchmarks on a risk-adjusted basis. The second table, in particular, makes clear that active managers are not simply unlucky — they are taking on additional risk that is not being rewarded.3

What makes 2025 especially instructive is that this was supposed to be the year active managers finally had their moment. Heading into 2025, some of Wall Street’s most prominent voices declared that conditions were ideal for stock picking. Goldman Sachs published a piece in February 2025 titled “U.S. Equities Are Ripe for Stock Pickers,” with chief U.S. equity strategist David Kostin arguing that high single-stock dispersion, low correlation, and elevated policy uncertainty created “a favorable backdrop for stock pickers.”6 Morgan Stanley’s Global Investment Committee published a piece in June 2025 titled “It’s a Stock Picker’s Market,” contending that U.S. tax legislation and financial deregulation would drive wide return disparities across stocks and that “active investing remains crucial.”7 LPL Financial’s research team pointed to rising dispersion and falling stock correlations as signs that “investors may benefit from active management, selective stock picking, and sector-rotation strategies.”8 The conditions — tariff volatility, high dispersion, a potential broadening beyond mega-cap tech — genuinely seemed to support the thesis.

And yet, 79% of active large-cap managers still lost to the index. It is a perfect illustration of why the case for passive investing doesn’t rest on predictions about conditions — it rests on 25 years of evidence that those predictions never reliably translate into active outperformance.

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett

What This Means for Your Plan

We have said it many times, and we will keep saying it: we are goal-focused, plan-driven, long-term equity investors. Our portfolios are built around your most important lifetime objectives — not around the futile pursuit of trying to find the next outperforming manager, or predicting which sector will lead next quarter.

The SPIVA data reinforces three convictions that are central to how we manage your wealth:

Low-cost, broadly diversified index funds are not a compromise. We believe they are a mathematically sound strategy for the overwhelming majority of long-term investors. Twenty-five years of evidence supports our view.

Past outperformance predicts virtually nothing about future outperformance. A manager who beat the benchmark last year is no more likely to beat it next year — and the longer the period, the more this truth asserts itself across every category we track.

The tariff-driven selloff of early 2025 — when the S&P 500 briefly fell more than 20%9 from its February high — was precisely the kind of moment when investors are tempted to flee to an “expert” who can supposedly navigate the storm. As we wrote to you then: the best course of action was to stay the course. The market recovered to record highs. The active managers trying to time that recovery mostly got it wrong and were left behind.

Nick Murray, whose work on investor behavior has profoundly influenced our philosophy, puts it simply: “The greatest risk for long-term investors is not short-term volatility, but failing to achieve their long-term goals.”10 Pursuing active management — which often involves higher fees, turnover, taxes, and potential uncertainty — can increase the likelihood of that risk.

The 2025 SPIVA Scorecard is the latest page in a 25-year ledger. That ledger is unambiguous. We believe in owning great companies, broadly and efficiently, for the long term — and in helping you remain invested through every storm so that the extraordinary power of compounding can do what it has always done.

Crises end. Markets recover. The patient investor wins.

We welcome your questions, as always. Thank you for trusting us to be your partner on this journey.

Warm regards,

Brendan McEwan, CFP®, CIMA®

Senior Financial Advisor

[1] YCharts, Performance of S&P 500 Index as calculated from close on April 8, 2025, through close on April 24, 2026. Investors cannot directly purchase an index.

[2] YCharts, Performance of MSCI EAFE Index as calculated from close on April 8, 2025, through close on April 24, 2026. Investors cannot directly purchase an index.

[3] SPIVA® U.S. Scorecard, Year-End 2025. S&P Dow Jones Indices LLC, CRSP. Data as of December 31, 2025. Past performance is no guarantee of future results. Investors cannot directly purchase an index.

[9] Yahoo Finance. Performance of S&P 500 Index as calculated from intraday high (6,147) on February 19, 2025, through intraday low (4,835) on April 7, 2025. Investors cannot directly purchase an index.

[10] Nick Murray, Simple Wealth, Inevitable Wealth. The Nick Murray Company, Inc. Referenced quote is widely attributed to this work.

RZH News: RZH Advisors and Carl Zuckerberg Earn National Recognition

RZH Advisors is proud to be named one of USA Today’s Top Financial Advisory Firms1, for the second year in a row, reflecting our continued commitment to enabling clients to embrace life to the full extent of their wealth.

These achievements are a true team effort! We are grateful to our colleagues for their hard work and shared commitment to positive outcomes, and to our clients for their continued trust and partnership. It is a privilege to serve as your trusted advisor, helping navigate complex financial decisions through the uncertainties of life.

[1]USA Today Best Financial Advisory Firms 2026 was published on April 14, 2026, in partnership with USA Today and STATISTA. Companies were awarded based on performance and market appreciation, evaluated in part via an independent survey among over 30,000 clients, industry experts, and constituents. In total, the top 1,000 firms out of over 15,000 RIAs were included in the ranking. No compensation was exchanged in consideration for this ranking.

[2] Barron’s Top 1,500 Financial Advisors was published on March 20, 2026, based on assets under management, revenue produced for the firm, regulatory record, quality of practice, and philanthropic work as of September 30, 2025. The data used in this ranking is provided by individual advisors in conjunction with regulatory databases. No compensation was exchanged in consideration for this ranking.

[3]Forbes 2026 Best-in-State Wealth Advisors was published on April 7, 2026, in partnership with Forbes and SHOOK research based on data as of December 31, 2025. Full ranking methodology can be found here. No compensation was exchanged in consideration for this ranking.

RZH Insights: When the Noise is Loudest, the Plan Matters Most

Is your head spinning and your stomach upset given today’s news cycle? You’re not alone.

In just the first ninety days of this year, we have witnessed an extraordinary convergence of economic, political, and market events – each one, on its own, capable of unsettling most investors. From geopolitical conflicts and unexpected policy developments, to sharp rotations within equity markets, surprise economic data, and moments of outright panic driven by speculative forecasts – the backdrop has been, by any measure, chaotic.

The United States undertook a highly unconventional geopolitical action, removing Venezuela’s president from power and detaining him on U.S. soil.

The U.S. administration publicly entertained the strategic acquisition of Greenland.

The Supreme Court invalidated key tariff measures enacted under emergency economic authority.

The price of Bitcoin declined by 50%, reinforcing both its volatility and uncertainty surrounding its role as a reliable store of wealth1.

The opening stages of the midterm election cycle began, introducing the potential for a meaningful shift in Congressional control.

Equity markets experienced a pronounced rotation from growth to value with AI euphoria shifting from unbridled optimism to worrisome distrust.

Civil unrest intensified across the country, culminating in fatal and widely covered confrontations between federal agents and protesters in Minneapolis.

A little known researcher, suggesting the possibility of severe economic contraction and unemployment levels of 10%, triggered a sharp, albeit temporary, bout of market anxiety2.

Silver prices surged dramatically before experiencing a historic one-day collapse of 35%3, underscoring the speculative nature of the commodity markets.

The United States and Israel dismantled leadership in Iran, contributed to the effective closure of the Strait of Hormuz, and drove a significant spike in oil prices.

“Private Credit” often-believed to be an exclusive asset class of the wealthy and institutions began weakening and faced massive redemptions4.

A YouTube journalist uncovered what appeared to be extensive fraud in Minnesota and California, revealing evidence of widespread misuse of taxpayer funds and prompting public scrutiny5.

Financial journalism once again pronounces that there is “no end in sight”.

And yet the US stock market is only down about 5% for the year, after doubling from just over three years ago6.

The Illusion of Urgency

Periods like this create a powerful – and very human – urge to act. To “do something.” To adjust. To protect.

This instinct is not irrational. It is simply misplaced.

The reality is that markets are always processing uncertainty. What changes is not the presence of risk, but the intensity of the narrative surrounding it. Today’s headlines feel urgent because they are delivered with relentless frequency and amplified emotion.

But here is the critical distinction:

Current events feel unprecedented in the moment – but they are entirely consistent with history.

NONE of the crises that I have written about over the last two decades kept the stock market from attaining an all-time high – JUST TWO MONTHS AGO7.

And that is why we should never make rational long-term investment policy out of current events.

The Core Principle: Plans, Not Predictions

At RZH, we operate from a foundational belief:

Long-term investment success is not achieved by reacting to current events. It is achieved by executing a disciplined plan – which accounts for interim risk and volatility.

Your financial plan was not built assuming only calm markets. It was built precisely for moments like this.

It reflects:

Your near-term needs and long-term objectives

The time horizon required to achieve them

The liquidity needed to ensure full attainment of these objectives

The historical realities of market returns – including volatility and bear markets

A diversified portfolio designed to protect short-term needs and capture premium returns over time

None of those inputs have changed. What has changed is the level of noise.

Why Reacting Fails

No advisor – no matter how experienced – can consistently predict:

The path of the economy

The occurence or resolution of geopolitical events

The short-term direction of markets

More importantly:

Even if one could predict these events, translating that into consistently successful portfolio decisions is virtually impossible.

History is unequivocal on this point.

Investors who attempt to navigate each crisis:

Tend to sell when uncertainty is highest

Miss recoveries that occur unexpectedly and rapidly

Ultimately compromise the long-term outcomes their plans were designed to achieve

When you have a sound, well-designed plan, volatility is not the risk. Reacting to volatility is.

What This Moment Is Teaching Us

If there is value in today’s environment – and there is – it lies in this:

It reinforces the futility of building investment policy around current events.

Markets do not reward anxiety – They reward discipline.

Historically, markets do not compensate reaction – They compensate patience.

And markets have historically transferred wealth from those who act on fear…to those who remain aligned with a thoughtful plan.

Our Guidance

At moments like this, our role is not to predict outcomes. It is to provide clarity, perspective, and discipline.

Which leads to a simple directive:

Stay aligned with your plan

Discount the noise

Maintain perspective

Allow time – and markets – to reward patience

Closing Thought

Periods of heightened uncertainty test conviction. But they also reaffirm what has been true:

There have historically been few (if any) asset classes (or any financial vehicles) that have generated real wealth as reliably and as effortlessly as have mainstream American common stocks.

We believe the most reliable path to long-term financial success and capturing the premium returns of common stocks is not reacting to the world as it unfolds – but remaining committed to a plan designed to endure it.

As always, we are here to guide you through it – with clarity, discipline, and confidence.

Best regards,

Carl J. Zuckerberg, CFP®, AIF®, CIMA®

Principal, Chief Investment Strategist

PS – Make sure to look for Brendan McEwan’s upcoming RZH Insights which outlines our approach and philosophy regarding how to best invest in equities over time.

[1] Yahoo! Finance. Decline calculated using BTC as measured from October 6, 2025 ($126,198) through February 28, 2026 ($63,062).

[6] Yahoo! Finance. “US Stock Market” 5% decline calculated using performance of Vanguard S&P 500 ETF (“VOO”) from January 1, 2026 ($627.13) through March 31, 2026 ($597.55). “Doubling over three years” calculated using performance of VOO from October 12, 2022 ($312.90) through December 31, 2025 ($627.13). Investors cannot directly purchase an index.

[7] Yahoo! Finance. S&P 500 Index closed at 7,002.28. Investors cannot directly purchase an index.

RZH Insights: Investment Optimism for 2026 and Beyond

2025 marked another year dominated by alarming, distressing and fear-driven headlines. A wall of worry was ever-present even though the stock market climbed nearly 18% 1 – an outcome that surprised most but was entirely consistent with my expectations. Over the years, many have asked me a version of the same question:

“Why are you always so optimistic about the stock market?”

It’s a fair question, especially in a world that feels perpetually unsettled. Markets swing. Headlines scream. Fear is amplified. Pessimism often masquerades as prudence. Optimism, on the other hand, is frequently dismissed as naïve.

But when it comes to long-term investing, optimism isn’t a personality trait – it’s an acknowledgment of reality and…

OPTIMISIM IS THE ONLY REALITY for investing in the world today.

The Market Is a Forward-Looking Machine

The stock market is less a report card on today’s economy – rather it’s a living, breathing forecast of tomorrow’s world. And when you look at history honestly, one truth stands out clearly:

Human progress consistently outpaces our imagination and expectations.

Innovation rarely arrives in neat, predictable increments. It comes in waves – often faster, broader, and more transformative than anyone expects. The technologies that end up reshaping our lives and our economy are almost always underestimated in their early stages.

Why?

Because people tend to extrapolate the present rather than imagine what’s next. That gap between imagination and the present matters enormously for investors.

Innovation Is Chronically Underpriced

Most people are very good at seeing today’s problems and very bad at envisioning tomorrow’s solutions. As a result, innovation is almost always underpriced by the market before it becomes obvious.

Consider:

We struggle to imagine new products before they exist

We underestimate productivity gains before they compound

We discount breakthroughs because they don’t yet fit into familiar models

And yet, time and again, innovation redefines what’s possible – economically, socially and financially. The companies that ultimately drive long-term market returns are rarely the ones that look comfortable or are fully understood at the outset. They are born from experimentation, risk-taking, and relentless problem-solving.

Markets, like people, struggle to price what they cannot yet fully imagine.

This persistent underestimation of innovation is not a flaw – it is an opportunity. It is one of the primary reasons long-term equity investors are rewarded.

Volatility Is the Price of Progress

Short-term market volatility often reflects uncertainty about how progress will unfold – not whether it will. Innovation is disruptive by nature. It challenges incumbents, upends assumptions, and forces constant adaptation.

That process can feel chaotic in the moment.

But zoom out far enough, and the direction becomes unmistakable.

Over long periods, markets don’t move higher because conditions are calm.

They move higher because productivity improves, efficiencies increase, and human ingenuity continues to advance and solve problems. All of this leads to increased capital formation and eventual wealth creation.

Why RZH Remains Disciplined

At RZH Advisors, our philosophy is grounded in a simple but powerful conviction:

The future will be more innovative, more productive, and more capable than the present.

That belief isn’t blind optimism or wishful “Hope” – it’s an observation supported by centuries of evidence.

Trying to time optimism – to wait until a new idea or innovation feels “safe” or fairly priced – has historically meant missing the very returns that drive long-term wealth creation.

The greatest investment risk isn’t short-term volatility or uncertainty.

It’s failing to participate in progress or disengaging from the process when volatility (fear) spikes.

The RZH Perspective

As long as people continue to imagine, invent, and improve, the long-term case for equities remains intact. And as long as innovation continues to surprise us – as it always has – those willing to stay invested will continue to be rewarded.

That is why we stay invested.

That is why we remain disciplined.

That is why we stay patient.

And that is why optimism remains the most rational long-term investment strategy of all.

All of us at RZH Advisors are excited about experiencing 2026 with you and being amazed at what’s next! May this year be your best ever!

Thank you, as always, for your continued trust and partnership.

Carl J. Zuckerberg, CFP®, AIF®, CIMA®

Principal, Chief Investment Strategist

P.S. Fortunately, there are a continuous number of bold, imaginative, enterprising people thinking about the future. If you want to be inspired about what’s next, just click on a few of these links which highlight the best inventions and breakthroughs of 2025:

[1] S&P 500 Index performance (Total Return including dividends) as measured from January 2, 2025, through December 31, 2025. Yahoo Finance. Investors cannot directly purchase an index.

RZH Insights: Mid-Year-ish Update and Timely Perspective

Every year brings its own surprises and uncertainties, and 2025 is no exception. While I will address recent events shortly, it is worth beginning with a reminder of the enduring principles that anchor successful wealth management. These guiding truths continue to shape our approach in working toward your objectives.

GENERAL PRINCIPLES

We are goal-focused, plan-driven, primarily long-term equity-oriented investors. Our portfolios are derived from, and driven by, your most important lifetime financial goals, not from any view of the economy or the markets.

We don’t believe the economy can be consistently forecast, or the markets consistently timed. Nor do we believe it is possible to gain any advantage by going in and out of the stock market, regardless of current conditions.

We therefore believe that the most efficient method of capturing the full premium compound return of equities is by remaining fully invested. We believe that even in challenging periods, reinvested dividends and disciplined portfolio rebalancing allow us to purchase more shares at lower prices – positioning you to benefit from the long-term power of equity compounding.

We believe that the greatest risk for long-term investors is not short-term volatility, but rather, not achieving your long-term goals.

CURRENT COMMENTARY

Ho-Hum, the stock market is already up over 10% this year, just like five of the last six years!1

If you looked at the stock market on the first trading day of this year, and not again until today, you could be forgiven for concluding that not much, if anything, had happened. In fact, a great deal has happened – but at least, so far, to no lasting effect.

The S&P 500 Index reached a new all-time high on February 19th.2 By April 7th, it had fallen 21%3 (on an intra-day basis). And even that doesn’t express the degree of sheer panic (there’s no other word for it) that enveloped the markets upon President Trump’s announcement (on April 2) of a dramatically increased tariff protocol.

The panic ended abruptly after President Trump announced a 90-day postponement of most of the new tariffs. In the months that followed – buoyed by continued economic strength and signs of moderating inflation – the S&P 500 Index returned to record highs, rising an astonishing 33% from its April 7th low.4

As it virtually always is, the optimal course of action for long-term investors was simply to continue following your plan. That’s what we encouraged our clients to do. And as the second half of the year continues, that recommendation stands. Please don’t mistake this for an economic or market outlook. We have no such forecast for the next five months, any more than we did on January 1st.

Our only forecast is that the excellent companies in our portfolios will continue managing challenges and innovating over time – increasing their earnings, raising their dividends, and supporting our client’s pursuit of their long-term goals.

Panic doesn’t often seize the investing public as suddenly as it did in the first week of April, nor vanish as suddenly as it did the following week. Still, this episode can and should serve as a tutorial.

Its lesson: investors succeed over time by consistently following their plan regardless of the latest “crisis.” Others often fail by reacting to negative events and liquidating even the highest quality stocks (great companies) at panic prices. We believe this is a fundamental choice in investing (and our mission, which we cherish) to help you continue making the wise choice.

PERSPECTIVES IN TIMES OF UNCERTAINTY: LESSONS FROM THE ‘70S AND TODAY

For many of us, the 1970s evoke memories of turmoil – economically, politically, and geopolitically. Inflation surged. President Nixon severed the link between the U.S. dollar and gold. The S&P 500 Index lost nearly half its value between 1973 and 19745 and didn’t reclaim its previous high for the better part of a decade. The oil embargo, Watergate, Vietnam, and a deep recession defined an era widely regarded as a “lost decade” for investors.

The President, the Federal Reserve and US fiscal policies were held in low regard. Sound familiar?

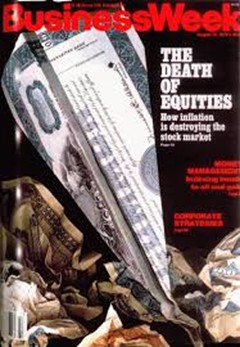

Business Week even declared “The Death of Equities” on its cover on August 13, 1979 – proclaiming that we should “regard the death of equities as a near-permanent condition”.6

But history is often more nuanced than headlines allow. While investors saw stagnation and political turmoil on the surface, a quiet revolution was unfolding beneath.

Just months after the gold standard was abandoned in 1971, Intel introduced the first commercially available microprocessor laying the foundation for the computer revolution.7 By 1975 and 1976, Microsoft and Apple were born – companies now valued at a combined $7.3 trillion.8

In hindsight, it’s a profound reminder: innovation doesn’t wait for calmer waters. It advances – even in the face of fear, volatility, and skepticism. Sometimes the most transformative opportunities are often born during periods of maximum discomfort – think AI (Artificial Intelligence) recently.

For those who remained invested, the results were extraordinary. From the time of that infamous magazine cover in August 1979 through July of this year (46 years) the S&P 500, assuming dividends were reinvested, compounded at 12.01% annually. In other words, a $1,000,000 investment would have grown to $184,000,000 (excluding taxes).9Take a moment and re-read that last sentence. Now read it again!

For most of our clients, the majority of their beneficiaries will easily live for another 46 years. At RZH we are not investing for “what will happen next”, we are investing for what will ultimately happen over the balance of your investing lifetime – and beyond, to the extent that legacy and generational wealth is part of your plan.

Crises end. Markets recover. Innovation endures.

Today’s headlines may be unsettling, but for investors with vision, discipline, and a structured plan, they need not be paralyzing. Our role as your advisors is to help you look past the noise – focusing not on what may happen next, but on what is most likely to unfold over the course of your financial life and legacy.

As Winston Churchill once said, “The farther backward you can look, the farther forward you can see.”

Let’s continue to look forward – together.

We welcome your comments and questions. Thank you, as always, for being our clients. It is a privilege to serve you.

May you be enjoying a wonderful summer,

Carl J. Zuckerberg, CFP®, AIF®, CIMA®

Principal, Chief Investment Strategist

[1] Total Return of S&P 500 Index assuming dividend reinvestment from January 1, 2025, through August 12, 2025. Investors cannot directly purchase an index.

[2] Yahoo Finance. S&P 500 Index intraday high (6,147).

[3] Yahoo Finance. Performance of S&P 500 Index as calculated from intraday high (6,147) on February 19, 2025, through intraday low (4,835) on April 7, 2025.

[4] Yahoo Finance. Performance of S&P 500 Index as calculated from the intraday low (4,835) on April 7, 2025, through market close (6,445.76) on August 12, 2025.

[5] Yahoo Finance S&P Index Historical Data. S&P Index return calculated from market close (120.24) on January 11, 1973, through market close (62.28) on October 3, 1974.

[8] Yahoo Finance. Combined market capitalization of Microsoft Corporation (MSFT: $3.91T) and Apple Inc (AAPL: $3.44T) as of August 12, 2025.

[9]S&P 500 Index Historical Calculation of 12.01% for the average of closing prices for the month of August 1979 through the month July 2025. Depicted investment performance assumes dividend reinvestment. For illustration purposes only, an investor cannot directly purchase an index.

RZH Insights: The More Things Change, the More the Stock Market Stays the Same

It’s hard to believe, but it’s been a year since Donald Trump and Joe Biden stood on stage in Atlanta, on June 27, 2024, for what would become their first – and only – debate.

What followed reshaped the American political and cultural landscape in ways few could have predicted. Since then, the national conversation has been dominated by words like “chaos” and “turmoil”. Cries of “this time it’s different” rained down from the pundits. It’s easy to understand why many felt this way when you consider the myriad events during the past 12 months:

Joe Biden withdraws from the presidential election

Donald Trump survives two assassination attempts

A global stock market decline wipes out $6.4 Trillion1

Climate Crisis hits new highs with catastrophic global natural disasters

Ukraine–Russia conflict intensifies

Israel-Hamas conflict continues

Donald Trump decisively wins the presidency

AI reshapes business and threatens millions of jobs

Elon Musk and DOGE turn DC agencies inside-out

President Trump imposes unprecedented tariffs

The S&P 500 index falls 21% in less than three months2

President Trump calls for the removal of Federal Reserve Chair Jerome Powell

Moody’s downgrades U.S. debt rating as national debt levels hit all-time high3

ICE raids and deportations divide America

Active-duty Marines deployed on U.S. soil to manage riots in Los Angeles

Israel attacks Iran

“No Kings” Day protests sweep the country

America enters the Israel-Iran conflict by bombing Iranian nuclear sites

The uncertainty, fear, and alarming headlines have been so overwhelming that I felt compelled to reflect on their emotional and psychological toll – in this recent newsletter, where I wrote about the impact these events have had on our clients, on me, and on our firm.

And yet, over arguably one of the most chaotic, emotionally charged and unpredictable 12-month periods in recent history, the S&P 500 rose 13.3%!4 An annual return ABOVE historical averages.5

How is that even possible?

The answer, as I’ve said countless times, and with deep conviction, is remarkably simple:

This time isn’t different: stock prices follow earnings – not headlines.

Great companies adapt. They find ways to navigate challenges, innovate through adversity, and create long-term value for shareholders. Over time, the stock market isn’t reacting to the noise of headlines – it’s responding to the enduring profitability of the companies it reflects.

So, the S&P 500 rose 13.3%, care to take a guess as to how much corporate earnings rose? Up 13.4%.6 Coincidence? Hardly!

As evidenced by this chart, this dynamic has been true for over 80 years. Stock prices follow earnings. The market doesn’t rise because the world is calm – it rises because great businesses keep delivering results. That’s the power of disciplined investing. That’s the power of focusing on fundamentals and having a plan to carry you through.

In other good news, the past 12 months also saw positive developments in several other high-profile areas:

Overall Inflation (CPI) – down 27%7

Price of Oil – down 20%8

Price of Eggs – down 25%9

Average price of a Taylor Swift concert ticket – down 29%10

Price of Bitcoin – up 56%11

YOUR FUTURE IS OUR MISSION

All of us at RZH work tirelessly to protect you and your loved ones. We will get through this together and continue to prosper. We’ll continue to carefully manage your plan behind the scenes, so please try to live tomorrow like you lived today – you’ve earned and deserve it.

[2] Performance of S&P 500 Index as measured from intraday high (6,147) on February 19, 2025, through intraday low (4,835) on April 7, 2025. Yahoo Finance. Investors cannot directly purchase an index.

Fraud and financial scams are becoming increasingly common, and even the most vigilant individuals can become targets. Understanding the risks and taking proactive measures can help safeguard your assets and personal information. Below, we outline common fraud schemes along with key steps to protect yourself.

Common Fraud Schemes & Warning Signs

1. Phishing Scams (Email & Text Fraud)

Example: A client received an email appearing to be from their bank, requesting account verification via a link. The email led to a fake website designed to steal login credentials.

Warning Signs:

Emails or texts with urgent language (e.g., “Your account will be locked!”).

Links that direct you to an unfamiliar website.

Unexpected requests for personal information.

How to Protect Yourself:

Never click on links in unsolicited emails or texts; go directly to the company’s website.

Verify the sender’s email address carefully.

If in doubt, call the institution using a known phone number.

2. Social Security & Government Impersonation Scams

Example: A caller claimed to be from the Social Security Administration (SSA), stating that the recipient’s SSN had been compromised and needed verification immediately.

Warning Signs:

Calls or messages claiming you must verify personal details immediately.

Threats of arrest, account suspension, or legal action.

Requests for payment via gift cards, wire transfers, or cryptocurrency.

How to Protect Yourself:

The SSA, IRS, or other government agencies will never call asking for personal info or payments.

Hang up and report the call to www.ssa.gov or the FTC.

Never share personal information over the phone unless you initiated the contact.

3. Fake Tech Support Scams

Example: A pop-up appeared on a person’s computer warning them of a virus and urging them to call “Microsoft Support.” A scammer convinced them to allow remote access and stole financial information.

Warning Signs:

Unexpected pop-ups warning of a virus and asking you to call a number.

Callers claiming to be from Microsoft, Apple, or Google offering to “fix” your device.

Requests for remote access or payment for unnecessary services.

How to Protect Yourself:

Legitimate tech companies will never proactively reach out about issues.

Never allow remote access to someone you don’t know.

Restart your computer and run a virus scan instead of engaging with pop-ups.

4. Fake Check & Overpayment Scams

Example: A seller on Facebook Marketplace was sent a Zelle payment for more than the item’s price and asked to send back the difference. The payment bounced after the seller returned the difference, leaving them responsible for the lost funds.

Warning Signs:

A buyer sends a check or Zelle for more than the agreed price.

Requests to return excess money via wire transfer or gift cards.

Checks that take a long time to clear (often fake).

How to Protect Yourself:

Never accept overpayments

Wait for funds to fully clear before withdrawing or sending funds.

Always verify the recipient and use caution when sending money electronically

5. Romance & Online Relationship Scams

Example: A client met someone on a dating site who quickly professed love and asked for money to help with an emergency. They later discovered the entire relationship was a scam.

Warning Signs:

A new online connection quickly becomes serious and emotional.

They always have an excuse for why they can’t meet in person.

Requests for money due to a sudden “emergency.”

How to Protect Yourself:

Be skeptical of online relationships that escalate quickly.

Never send money to someone you haven’t met in person.

Reverse image search their photos to check if they appear elsewhere online.

Key Steps to Protect Yourself from Fraud

Enable Two-Factor Authentication (2FA): Add an extra layer of security to your email, bank accounts, and financial institutions.

Enroll in a Credit Monitoring Service: Services like Equifax, TransUnion, or Experian can alert you to suspicious activity and prevent identity theft.

Place a Security Freeze on Your Credit: This restricts access to your credit report, making it harder for fraudsters to open accounts in your name. You can unfreeze it when needed.

Be Cautious with Personal Information: Never share sensitive details like your Social Security number, date of birth, banking information, or passwords unless you are 100% sure of the recipient. Never email this information unless using an encrypted or secure method.

Verify Requests for Money or Information: If a request seems urgent or unusual, take a step back (talk to a friend or loved one) and confirm its legitimacy before acting.

Final Takeaway: Stay Vigilant, Stay Secure

Scammers rely on urgency, secrecy, and emotional manipulation to trick people into acting quickly. This is not an exhaustive list of fraud schemes or protective measures, but it provides a strong foundation for keeping your personal and financial information secure. By staying informed and taking proactive security measures, you can significantly reduce your risk of falling victim to fraud. If you ever have concerns or suspect fraudulent activity, reach out to us immediately. We take the security of your financial future seriously and are always here to help.

Warmest Regards,

Lauren Rowland CFP®CDFA®

RZH Insights: A True Test of Investor Resolve

What a remarkable time to be an investor. Depending on your perspective, the past five weeks have been either deeply unsettling or profoundly instructive. They’ve brought waves of panic – but also powerful reminders of timeless investment truths.

For me personally, this has been one of the most emotionally taxing periods of my 33-year career. It’s not the volatility – we’ve seen plenty of that before. What’s been most challenging is the level of fear and anxiety expressed by clients, even those with solid plans and well-constructed portfolios. The conversations I’ve had in recent weeks have often been emotional, very personal, sometimes painful, and a real test of my own resilience as an advisor.

Over the past month, markets have tempted investors into making the classic and costly mistake: abandoning their long-term strategy under the belief that “this time is different.” If you’re a client or friend of RZH, you know our firm is grounded in conviction – conviction in our disciplined planning and investment process. I have unwavering confidence in the great companies we invest in to navigate through the perennial problems, challenges and black swans that come our way, no matter how chaotic or unique they may appear. And while I have more tempered faith in government responses, I believe strongly in the resilience and adaptability of the global economy over time.

At RZH, we believe success in investing demands discipline, emotional detachment, and a long-term mindset. That doesn’t mean ignoring reality – far from it. Unpredictability and disorder seem to be embedded in this administration’s approach to policy and negotiation. Mynewsletter on April 4th recognized this and outlined our plan. The market continued falling and bottomed on April 7th. The very next day, we delivered this newsletter advocating caution and patience.

Since that low on April 7th the S&P 500 Index has surged more than 20%1 and the tech-oriented NASDAQ Index gained over 26%2 – both delivering two years’ worth of returns in just over a month. These dramatic reversals reaffirm everything we believe in: thoughtful goal-based planning, strategic allocation, and the importance of staying the course. The best market returns often directly follow the worst, and the timing of these turnarounds is virtually impossible to predict.

Of course, we’re not declaring victory – we are far from “out of the woods.” But we are more confident than ever in the durability of our investment philosophy and the strength of our client relationships. Our mission remains clear: to make market volatility irrelevant to your financial security, and to help you embrace life fully, supported by a plan built to weather any storm.

We don’t know what the next five weeks will bring – let alone the next five days. But what we do know is this: everyone at RZH is prepared, steadfast, and honored to be your trusted partner through it all.

Best regards,

Carl J. Zuckerberg, CFP®, AIF®, CIMA®

Principal, Chief Investment Strategist

[1] Performance of the S&P 500 Index as measured from the intraday low (4,835.04) on April 7, 2025, through market close (5,844.18) on May 12, 2025.

[2] Performance of the NASDAQ Index as measured from the intraday low (14,784.03) on April 7, 2025, through market close (18,708.34) on May 12, 2025.