This year marks a meaningful milestone for all of us at RZH Advisors — 25 years of trust, partnership, and shared success.

As we reflect on this journey, we’re reminded that our success has always been about people — our clients, colleagues, families, and community who have made the last 25 years so meaningful. Your trust and confidence have shaped who we are. While much has evolved over the years, our mission remains the same: to deliver thoughtful, personalized financial guidance and to keep your goals at the center of everything we do.

On behalf of the entire RZH Advisors team, thank you for allowing us to be part of your story. We look forward to continuing this journey with you in the years ahead.

JOIN US IN CELEBRATING 25 YEARS, WATCH OUR STORY:

RZH 25TH ANNIVERSARY CELEBRATION— SEPTEMBER 2025

In September 2025, RZH Advisors closed the office for two days to celebrate our 25th anniversary with a company-wide retreat at The Sagamore in Lake George, NY.

Our team members and their significant other were invited to join in the milestone event. We kicked off the celebration with a lively trivia night, designed to break the ice and setting the stage for a full day of activities showcasing our team spirit. The second day featured an immersive instructor-led scavenger hunt across the grounds, a celebratory luncheon, and a mix of organized activities including pickleball, golf, tennis, and the spa. The celebration concluded with a festive Hawaiian luau themed dinner, bringing everyone together to honor RZH’s history, and our incredible team members who made this milestone possible.

Finally, RZH provided team members the option to stay an extra night, extending their retreat and allowing unscheduled free time to enjoy the beautiful early fall season in Lake George.

Thank you for 25 years of trust, partnership, and shared success.

RZH Insights – The Stealth Bull Market

If a bull tiptoes through a china shop, does anyone know it’s there?

During mid-October, the U.S. stock market was undergoing a challenging bear market. Inflation rates remained high at nearly 8% annually1, and the Federal Reserve was actively increasing interest rates. At that time, both the S&P 500 and the Nasdaq 100 had experienced significant declines of over 25% and 35% respectively from their previous peaks1. The situation appeared grim, as there was no clear indication of a market recovery.

However, since mid-October, there has been a remarkable turnaround – one that we have been referring to as a “stealth bull market” due to the lack of press it has received. The rise has been lumpy and overshadowed by continued inflation news, Federal Reserve interest rate speculation, a banking crisis, US/China tensions, a debt ceiling emergency, and the Taylor Swift world tour.

From the October 2022 lows, the Nasdaq 100 has surged by an impressive 37%, while the S&P 500 has risen over 20%. Although the market is still below its all-time highs, this rally has defied predictions of a recession made by many experts over the past 18-24 months.

Now the question arises: Is the bear market over? Are we witnessing the start of a new bull market? As always, it is difficult to say for certain, considering the confusing nature of the stock market during such times. A prime example is the largest company in the U.S. stock market, Apple. Last summer, its share price nearly fell 30% from its all-time high, followed by a 36% rally, then dropped nearly another 30%, and is now approaching its peak once again with a 48%+ rally1. This is all in the span of 18 months!

These fluctuations demonstrate the back-and-forth nature of the market, with alternating bull and bear phases. While we may have technically reached the definition of a “bull market”, as the stock market is now 20% above its October 2022 lows, such classifications primarily matter only to market participants. The true answer can only be determined with the passage of time.

It is worth remembering that the renowned bull market of the 1980s and 1990s is commonly believed to have started in the early 1980s. However, from the end of the bear market in late 1974 until the end of 1979, the S&P 500 had already risen by nearly 120% in total or 16% annually1. This often goes unnoticed due to the challenging financial environment of the 1970s. Similarly, it took until 2013 for the S&P 500 to surpass its pre-Great Financial Crisis highs, despite having risen more than 150%, or about 25% annually, from the 2009 lows. In the end, does it truly matter whether these gains occurred during a technical bull market or just a bear market rally?

While it is not guaranteed that history will repeat itself, during the “lost decade” of the 2000s many individuals became conditioned to believe that every downturn would result in a catastrophe – as the media tends to espouse and continually reinforce. The same sentiment appears pervasive today. However, bear markets typically occur once every five years…so it is possible (actually quite common) to have a bear market without the world completely unraveling in the process.

No one can perfectly time market highs or lows. The emotions of panic during a downtrend and euphoria during an uptrend may be similar, but each bull and bear market has its own unique characteristics, making predictions challenging.

We never know how high a bull market will climb or how long it will last. Similarly, as illustrated in the chart below, we cannot anticipate how low a bear market will go or its duration. Even if we are currently in a new bull market, there is likely to be a pullback in the coming year. Over the past 43 years, the average intra-year decline has been about 14%2.

In terms of understanding bull and bear markets, it is important to recognize that the long-term trend is generally upward, but short-term downturns are inevitable. The lows are (and always have been) temporary and the highs are ever-reoccurring.

Our feelings remain unchanged…the economy cannot be forecast, and the markets cannot be timed. Having a plan is imperative and patience is always rewarded in investing. Our client’s financial plans are designed with the understanding that we will encounter various bull and bear markets throughout the years.

Together we will navigate these challenging times as well – by continuing to manage your plan, adhering to the principles of successful investing, and staying focused on your most cherished financial objectives. We are always here for you and encourage you to reach out at any time with questions or thoughts.

Thank you for being our clients, it is a genuine privilege to serve you.

1.Inflation data, S&P 500 Index performance, and NASDAQ 100 Index performance calculated for the period Jan 4, 2022 – October 12, 2022, using historical data sources from the Yahoo! Finance Historical Data tool. Apple performance calculated for the period Dec 2021 – June 2023. While we believe this data source to be reliable, its accuracy and completeness are not guaranteed. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security, and past performance is no guarantee of future results.

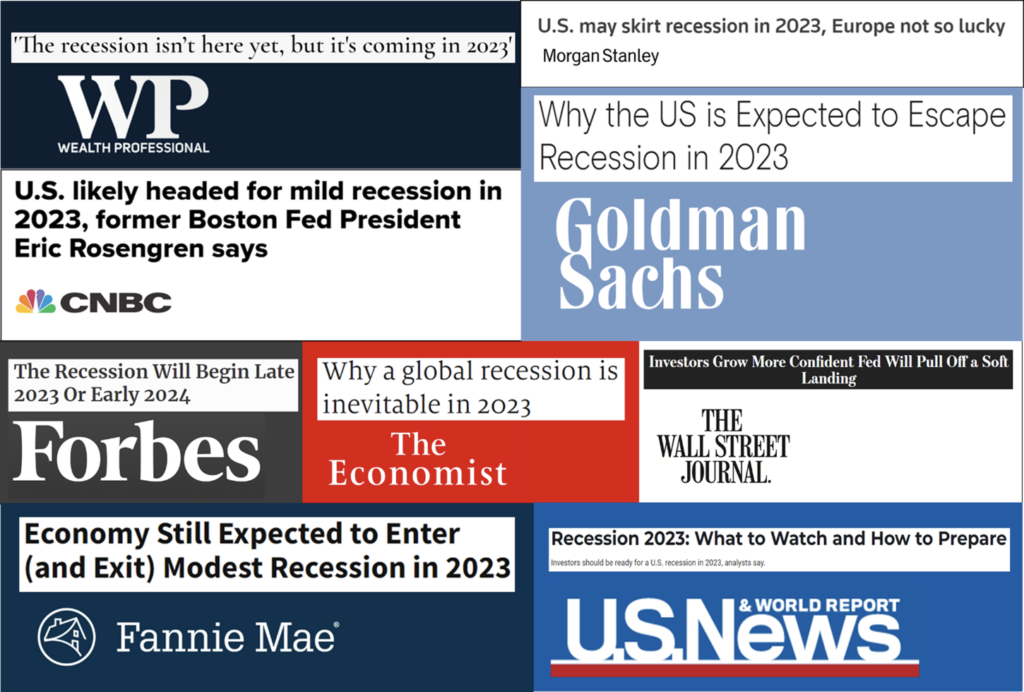

There have been a lot of headlines recently about the possibility of a recession in 2023. Here are a few examples:

As you can see, economic predictions for 2023 are all over the map as is often the case. As the saying goes, “economists have predicted 9 out of the last 5 recessions”. What’s interesting is that each prediction, which is about something so historically hard to predict, is said with such conviction that it leads you to believe the author’s opinion and wonder “what do they know that I don’t?”.

Predicting stock market returns is equally as challenging. “Expert” projections for 2022 (made at the end of 2021) ended up being far from reality. The median “expert” forecasts for the S&P 500 were about 26% higher than where it closed at year-end.1 The most bullish forecast was about 38% higher and the closest forecast was still about 15% higher than where the S&P 500 ended 2022.2 Let that sink in for a moment, the best projection of the top forecasters was off by 15%! That’s comparable to a meteorologist telling you it will be cold and snowing, but when you go outside it’s warm and sunny. If that happened consistently, you would not trust that meteorologist for long.

The argument as to why the projections of so many “experts” were off in 2022 is that “there were a lot of unpredictables last year.” The “unpredictables” were Russia’s invasion of Ukraine, China’s continued COVID shutdowns, persistent global inflation, and the energy crisis in Europe, among others. As we have previously stated, every year has its own exogenous variable du jour. It is often extremely difficult to predict and even harder to determine how the investment markets will react to these unforeseen events.

All of these events have led to the great debate of whether we will see a recession in 2023. As you can tell by the headlines above, there is no overarching consensus about whether or not a recession will occur, how bad it will be, how long it will last, if we are currently in one, or even what the definition of a recession actually is! But, even if there was a consensus, should we believe it? The most economically well-versed experts tried to predict what would happen in 2022 and missed by a mile.

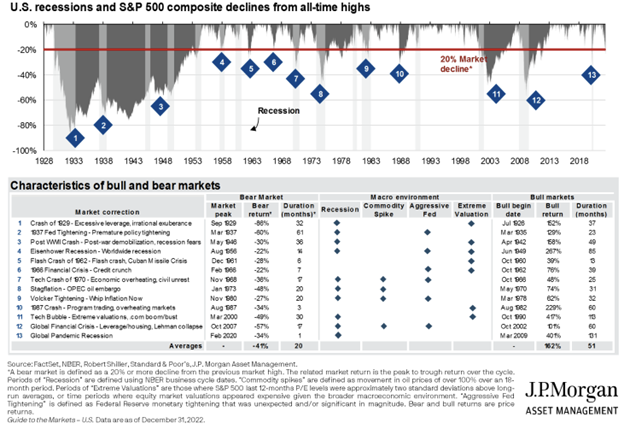

In reality, no one knows whether a recession will occur in 2023, 2024, or anytime thereafter. A broad definition of a recession is “a significant, pervasive, and persistent decline in economic activity.” Economists measure a recession’s length from the prior expansion’s peak to the downturn’s trough. By its definition, a recession is usually only determined AFTER it has already occurred. Recessions are not rare: economies are in a state of recession 10-12 percent of the time.3 Since The Great Depression in 1929, there have been 13 recessions, averaging out to about one recession every seven years. Each recession, its duration, return, and subsequent bull run is detailed in J.P. Morgan’s chart here.

In a recent article, Ben Carlson stated, “One thing is for sure – we are NOT in a recession right now. The 4th quarter of last year saw real GDP grow at an annualized pace of 2.9%. On the whole, the U.S. economy grew 2.1% in 2022 (even after accounting for inflation). Combine this with a 3.5% unemployment rate and it would be impossible to call the current environment a slowdown… Everyone has been worrying about a recession for more than a year now already so it’s not like these risks are unknown.” Perhaps this “inevitable” recession is already priced into the markets.4

If past predictions are any indication, 2023 will likely surprise us with results far from consensus. No one has ever been able to consistently predict what will happen in the economy. The only proven strategy to endure the ups and downs of the markets is to approach investing with a long-term and disciplined approach.

The investment markets are a forward-looking mechanism and often begin to recover before a recession is over. As Jeremy Seigel states in his famous book Stocks for the Long Run, “by the time the economy has reached the end of the recession, the stock market has already risen on average 25% from its low, therefore, an investor waiting for tangible evidence that the business cycle has hit bottom has already missed a very substantial rise in the market”.5

At RZH Advisors, we feel that adhering to our investment principles is especially important if you are faced with the uncertainties present in today’s markets. These principles are:

Faith in the Future – The investment markets have historically increased over long-time frames. Investing contrary to 200 years of history has proven detrimental.

Patience – Tolerating interim volatility allows markets to complete their full cycle. This allows different asset classes to benefit from historical performance patterns.

Discipline – Sticking to your financial plan by following time-tested strategies and investment management principles during times of maximum uncertainty.

Asset Allocation – Risk and return are related. The investment mix of stocks, bonds, and cash will be the primary determinant of portfolio return on a long-term basis.

Diversification – Being broadly diversified within each asset class further reduces risk without reducing potential returns.

Rebalancing – The disciplined art of systematically reallocating your portfolio back to its original target allocation. When implemented properly, the result is “buy low, sell high”.

We are here to help you navigate the uncertainties and the temptations of human nature which often provokes you to question these principles. Through our planning process, we design custom-tailored portfolios with a thoughtfully crafted balance of stocks, bonds, and cash for each client’s particular situation. While past performance does not guarantee future results, our portfolios are designed to support you through the challenges present in today’s market environment allowing you to continue to live the life to which you have grown accustomed. We achieve this by following our recession playbook which has been developed to mitigate the effects of market volatility: keep 1-2 years of cash flow needs on the sidelines, maintain 4-5 additional years of investment-grade short/intermediate-term bonds, and own predominately large-cap blue-chip stocks. It is equally important to consistently monitor your plan by employing strategies such as rebalancing, tax-loss-harvesting, investing available cash to take advantage of depressed stock prices, and avoiding large expenses when the market is down.

A recession, or a decline in the investment markets, does not imply a permanent loss in your portfolio. That can only occur if there is an imprudent reaction to headlines or volatility in the markets. RZH Advisors is here to help you navigate the challenges associated with maintaining a disciplined and successful investment experience.

Whether or not a recession occurs in 2023, our goal is to help you and your family reach your long-term goals. We are always here for you and encourage you to reach out at any time with questions or thoughts. Thank you for being our clients!

[1] Sommer, Jeff. “Forget Stock Predictions for Next Year. Focus on the Next Decade.” The New York Times, December 17, 2022. https://www.nytimes.com/2022/12/16/business/economy/stock-market-forecast.html.

[2] Goodkind, Nicole. “Wall Street’s Dirty Secret: It’s Terrible at Forecasting Stocks.” CNN, December 28, 2022. https://edition.cnn.com/2022/12/28/investing/premarket-stocks-trading/index.html.

[3] Investopedia. “Recession: What Is It and What Causes It,” November 17, 2022. https://www.investopedia.com/terms/r/recession.asp.

[5} Guide to Financial Market Returns & Long-Term Investment Strategies (6th ed.). McGraw Hill. Siegel, J. (2022). Tocks for the Long Run: The Definitive Guide to Financial Market Returns and Long-Term Investment Strategies

Last year was exhausting for investors. Even with 32 years in the business, and a passion for navigating the capital markets, I too was looking forward to putting 2022 in the rearview mirror. Last year brought unrelieved chaos as the hits just kept coming.The central drama of the year was the Federal Reserve’s belated but very aggressive efforts to bring inflation under control by aggressively raising interest rates.Other factors such as supply chain bottlenecks, the Russian/Ukraine war, China’s COVID lockdowns, the midterm elections, an energy crisis in Europe, and a historically strong dollar all created turmoil and kept volatility high.

For an illustration of the most 2022 market-moving headlines CLICK HERE.

For a complete review of 2022 global capital markets CLICK HERE.

After rising almost 700% in the nearly 13 years between the trough of the Global Financial Crisis (March9, 2009) and January 3, 2022, the U.S. equity market sold off sharply-declining 27% by mid-October.1 Bond prices also swooned in response to sharply higher interest rates, producing the single worst year in history for bond returns. 2022 was the worst year ever for US stocks and bonds collectively as illustrated HERE.The best news may be that, hopefully, the worst is behind us and historically the worst years are often followed by some of the best, especially after midterm elections and in the third year of a presidential cycle–as illustrated HERE.

Perspective

Even after taking a bruising last year and enduring the unprecedented challenges of the pandemic since early 2020, the S&P 500 managed to close out 2022 higher than it was at the end of 2019 (generating a total return of 24% over three years)1. Not bad for three years during which our entire economic, financial, social-political, and geopolitical world was turned upside down. This is especially impressive when you consider that over the same period, bonds lost 8%, real estate fell 2% and cash yielded almost0%.2

This tends to validate our core investment strategy, which-simply stated-has been to stand fast, tune out the noise and continue to work on your long-term plan. This continues to be my recommendation as our financial controls make it possible to avoid selling at depressed prices and avoid emotional trading.Selling when asset prices are depressed severely impairs the process of compounding. The stock market’s long-term annualized return of 10% was created by the blending of good years and bad. After many good years, we just had a bad one, as has happened numerous times before.

After a particularly trying year, let’s pause to quickly review our general investing principles:

We are long-term, goal-focused, plan-driven investors whose portfolios are equity-oriented for growth to sustain an inflation-adjusted standard of living, usually over decades and often to preserve assets for loved ones. We believe that lifetime investment success comes from acting continuously on a plan.Likewise, we believe substandard returns come from reacting to current events and not following a thoughtfully crafted plan–specific to your personal goals. The unforeseen and indeed unforeseeable economic, market, political and geopolitical chaos of the last three years demonstrates conclusively that the economy can never be consistently forecast, nor the stock market consistently timed. Therefore, we believe the most reliable way to capture the full return of equities is to ride out their frequent but historically always temporary declines. Our philosophy of keeping investment costs low, being tax efficient, rebalancing, and focusing on prudent cash flow management are all vital to long-term success.These will continue to be the bedrock convictions that inform our investment policy as we pursue your family’s most important financial objectives.

Moving Forward

Looking ahead, we will likely face many of the same risks and uncertainties of 2022. The burning question of the hour seems to be whether and to what extent the Fed, in its inflation-fighting zeal, might tip the economy into recession at some point-if it hasn’t already done so. Over the coming year, the way this plays out may determine the near-term trend of equity prices. Wall Street is quite divided on this, and, in my opinion, this most-anticipated recession in history may already be well-priced into the markets. (Brendan McEwan has penned a piece on this which we will deliver to you shortly.) The market will also be watching how the war in Ukraine plays out, how higher interest rates will affect consumers pending and company earnings, and the result of China’s shift away from its Zero-Covid policy. My position continues to be that these outcomes are simply unknowable and that one cannot make rational investment policy out of an unknowable. This strengthens our conviction to maintain our planning-driven investment process focused on achieving defined outcomes versus trying to tap dance around short-term erraticism.

That said, I continue to believe strongly that whatever it takes to put out the inflationary fire will be well worth it. Inflation is a destructive force that destroys wealth and economic progress. Temporarily delaying the next bull market to limit the damage is in everyone’s best interest. Just look at Paul Volcker’s actions in the early 80s which led to one of the greatest bull markets of all time.

The consensus among Wall Street strategists is that the first half of 2023 will bring continued volatility as the markets analyze the progression/resolution of the aforementioned global issues and the possible onset of a recession. However, most experts see the markets turning higher in the second half of the year as these issues hopefully abate and the markets price in better times ahead.

Don’t be surprised however if the markets turn higher well in advance of things settling down. This is normally how market recoveries start as the stock market is famous for generating a strong rally well before a recession is over and before Fed policymakers end their tightening cycle.

The Bottom Line

All of us at RZH look forward to seeing you as we conduct annual reviews over the next few months – even though the reports will not be as cheery as the past few years. Most importantly, please know that we hear you and understand how anxiety producing this past year(s) has been. You are not alone if you are worried about your finances, the world, and what 2023 might bring. If you are a client of RZH you know that we have prepared for the good and the bad, as well as stress-tested your plan. Our mission remains unchanged: to help you live an extraordinary life by maximizing your wealth. We work tirelessly to provide impactful counsel and planning such that market fluctuations are irrelevant to your financial security. We are always available to discuss any concerns you have. As I always say – but can never say enough – thank you for being our clients. It is a genuine privilege to serve you.

What goes down 12%, then up 11%, then down 20%, then up 17%, then down 9%, then up 5% then down 11%? You unfortunately already know the answer…it’s this year’s stock market! These are the actual movements since January 1st, leaving the S&P 500 down 22% for the year.

Are you exhausted yet? You are not alone, most RZH clients are as well.

For an explanation of why this is happening please refer to my Q2 memo HERE. Since then, we’ve had even worse inflation news and an even stronger response from the Federal Reserve which has triggered this latest downturn. The market is adjusting to higher interest rates, less liquidity, and the realization that the era of the “Fed put” is over.

Is there any precedent for this – yes:

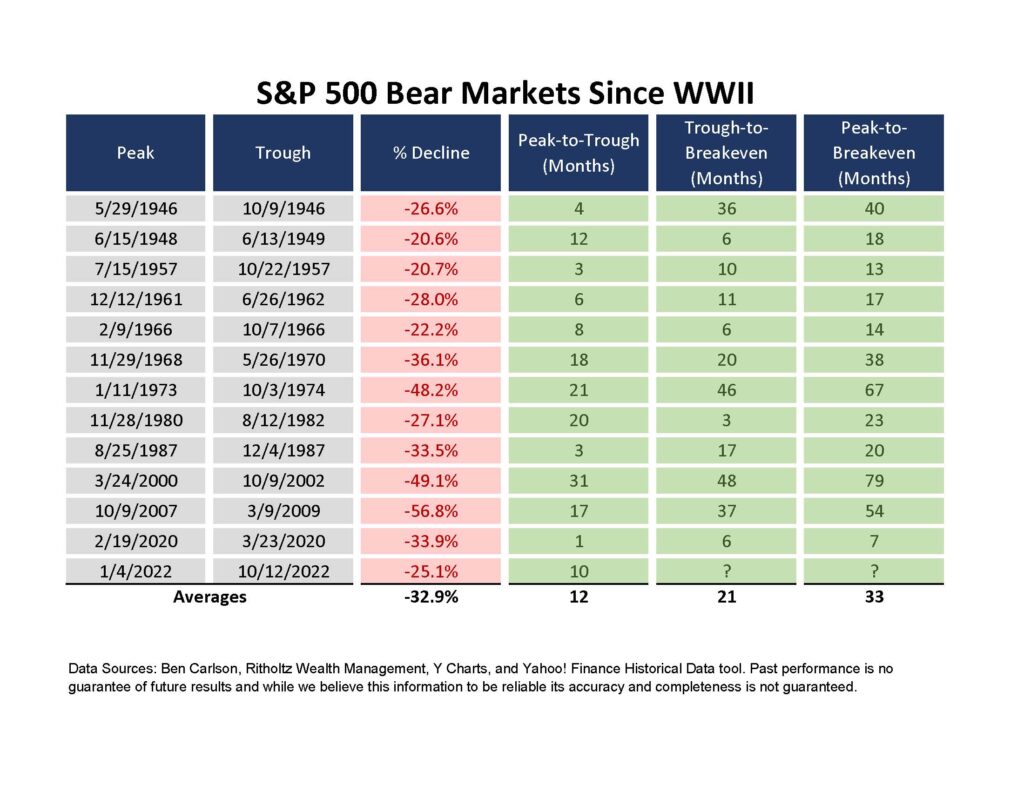

There have been 14 bear markets (including this one) and 13 recessions since World War II – an average of one about every 6 years.

The average bear market decline is -32.7% which implies that this bear market could see further downside. I would not be surprised to see this, especially given the myriad of global geopolitical risks, continued inflation surprises, and the Fed’s desire to remove liquidity from the system.

The good news is that the average bear market lasts 367 days, so we may already be 75% of the way through this one.

A silver lining is that you can finally earn some interest on cash and bonds. A two-year Treasury bond yields over 4% – up from .26% just a year ago

Each bear market and recession is unique in its own way. This one is unlike anything we’ve seen before given the confluence of the pandemic, excessive government stimulus, persistent inflation, European energy crisis, supply chain shocks, the Ukraine war, etc. Every bear market causes feelings of panic and despair. They make you question your investment plan and previously held investing beliefs. All bear markets are painful – every single one of them.

Emotions are running high, and an important part of our job is to help clients reject emotional responses in favor of rational decision-making. Bear markets are when individuals and families protect their long-term wealth and ensure a more predictable future by not panicking and instead sticking to a well-designed plan. Our clients have custom-tailored financial plans whereby each dollar invested has a specific role in achieving an important personal objective. The worst plan is the one not followed, especially in the face of provocation such as this market environment and media hysteria.

Neither I (nor any other honest person) knows when this will end, but we do know that it will end. To plan any differently would be ignoring 200 years of history. I believe that forming investment policy based on predictions, instead of evidence, is very dangerous.

In the meantime, it is more important than ever to follow the pre-mentioned bear market/recession playbook: keep 1-2 years of cash flow needs on the sidelines, maintain 4-5 additional years of investment-grade short/intermediate-term bonds and own predominately large-cap, blue-chip stocks. It is equally important to keep working on your plan by rebalancing, tax-loss-harvesting, avoiding large expenses when the market is down, and investing available cash to take advantage of depressed stock prices. For more on this please re-read Dana’s Three Bucket Theory memo HERE.

At RZH we’ve successfully navigated through many bear markets and recessions. I’m sure this won’t be the last. We are always here to talk this through with you and answer your questions. Thank you for being our clients. It is a privilege to serve you.

Best regards,

Extra content: The majority of our equity holdings are those which comprise the S&P 500 and their international counterparts. This is not a random set of stocks or merely a “passive” index. Unbeknownst to many, the S&P 500 is a thoughtfully selected and carefully managed portfolio of the largest, most soundly financed, best managed, most profitable, most innovative, and most transparent companies serving America and the world. For an insightful explanation of how to think about these stocks (versus the “stock market”) please click on THIS MEMO or ask me to walk you through a seminar I gave on this topic. The bottom line is that the long-term upward trend of stocks does not occur in a straight line. So, perhaps consider the accompanying volatility as simply the price of admission to owning an asset class that has produced compounded returns of 10% annually.

Some material, content, and statistics are derived from Ben Carlson’s blog A Wealth of CommonSense, and the Nick Murray Interactive newsletter

After rallying earlier this month the stock market sold off precipitously this last week, falling 10% in just five days, closing at its lowest point of the year on Tuesday. The latest route was triggered by a worse-than-expected inflation reading last Friday – the worst in 40 years. This initiated the frenzied selling of stocks and bonds as the market tried to comprehend where inflation and interest rates are headed. Interestingly, even gold (a typical inflation hedge) has declined recently. The message to me is that the capital markets have lost faith in the US Federal Reserve, as well as global central banks, to effectively tame inflation through monetary policy. It is clear – there is much uncertainty as to where global economies are headed.

To make things worse, during these periods of heightened volatility, the primary function of financial journalism seems to be terrifying us out of ever achieving our financial goals by shrieking about the market’s volatility. We’ve been reminded of this almost hourly as the S&P 500 approached “official bear market territory,” defined as closing 20% below its January all-time high.

Please know, we fully understand how unusually painful this has been. This year has seen the worst start for the stock market since 1939 and the worst start ever for bonds. We hear your concerns and feel your anxiety. As co-investors in all RZH investments, we are experiencing this downturn side-by-side with you as well.

Every market decline of this magnitude has its own unique precipitating causes. I think it’s fair to say that the current episode is a response to two issues: severe inflation, and the extent to which the economy might be driven into a recession by the Federal Reserve’s somewhat belated efforts to root that inflation out. (Russia’s war on Ukraine, supply chain issues, Covid lockdowns in China, and the like are surely contributing to the angst, but recession vs. inflation is the main event, in my judgment.)

Here is some perspective:

From March 2009 (when the equity market bottomed at the end of the Global Financial Crisis) through the end of 2021, the S&P 500 produced an average annual compound return of 17.5%. Indeed, over those last three calendar years (2019 – 2021), despite a hundred-year global health crisis that took the lives of millions of people worldwide, the Index compounded at 24% per year. This was one of the greatest runs of all time. (Remember, the long-term annual average return for stocks is only about 10%.)

However, it’s evident that some part of that extraordinary accretion in equity values was due to excessive monetary stimulation by the Fed. And to that extent, we are having to give some of that gain back, as the Fed moves to bring the resultant inflation under control. I consider this somewhat a process of reversion to the mean. We should, I believe, want them to do this, even if it means the economy slows. In the long run, the cure (possible recession) is not more painful than the disease (inflation). For long-term investors, capitulation to a bear market by fleeing equities has often proven to be a tragedy, from which their retirement plans may never recover. Our investment policy is founded on the acceptance of the idea that the only way to be reasonably assured of capturing equities’ premium returns (about 10% annually) is by riding out their occasional declines.

Short-term volatility is not risk, unless acted upon. Risk should be measured as the probability that we won’t achieve our goals. So, our mission continues: not to eliminate short-term volatility, but to provide a high probability of meeting your lifetime financial objectives. The playbook for these scenarios is proven throughout history: keep 1-2 years of cash flow needs on the sidelines, maintain 4-5 additional years of investment-grade short/intermediate-term bonds and own predominately large-cap – blue-chip stocks.

As this is exactly how RZH portfolios are currently positioned, I continue to counsel staying the course. This has been a winning formula for history’s most challenging economic environments. Sexy – no, effective – yes.

The good news…markets have usually rebounded well after periods of similar volatility (see chart)

We are always here to talk this through with you. Thank you for being our clients. It is a privilege to serve you.

RZH Insights – Practicing Rationality in the Midst of Uncertainty

Dear Clients and Friends of RZH,

After the S&P 500 Index rose 28.1% in 2021, the stock market cooled off and has slipped 4.6% in 2022 (as of March 31st). It must have been an uneventful quarter…right? Can you believe that after all the events of the past three months, the S&P 500 is only down about 4%?

On February 24th Russia invaded Ukraine. On that day, I sent a letter (which can be found here) discussing the events and our thoughts about your investment portfolio. One of the points I made discussed average intra-year drawdowns for the S&P 500. I want to reiterate this point because, thus far, 2022 has been playing out similar to historical norms.

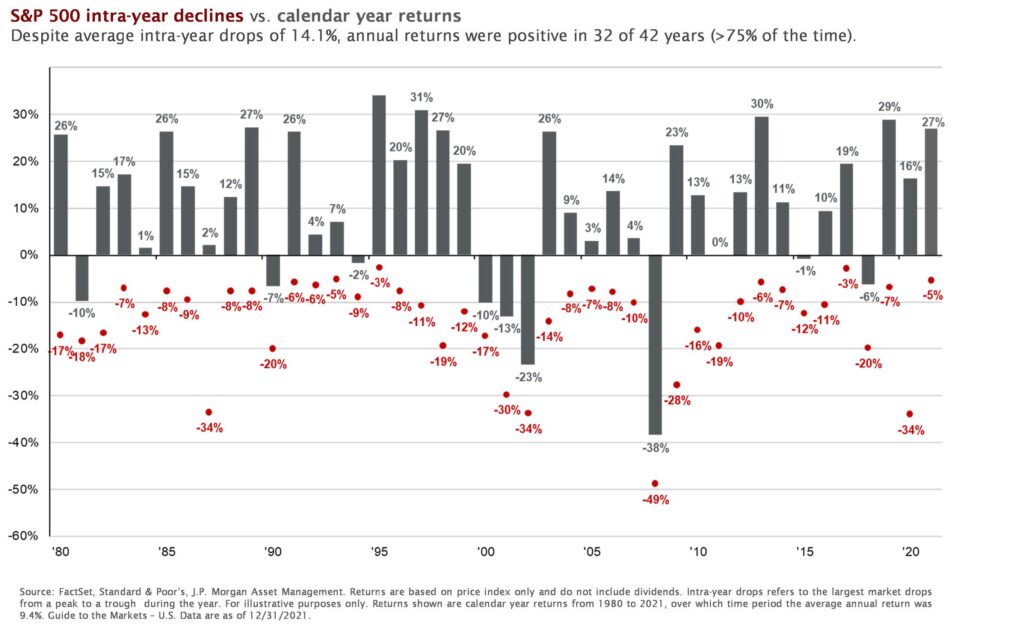

Since 1980, the S&P 500 index has exhibited average intra-year declines of 14.1%. Despite this, as shown in the below graph, the index has finished the year positive in 32 of the last 42 years (76% of the time) and produced an annual compounded return of 12.1%. This graph shows each year’s largest intra-year decline, represented by the red dot, and the return of the S&P 500 for each year overall, represented by the grey bar.

So far for 2022, the largest intra-year decline for the S&P 500 is -14.2%. This low happened on February 24th. While it is difficult to experience such a drop, this type of decline is in line with historic norms. Since the low on February 24th, the S&P 500 is up 10.1% (as of 3/31/2022). This shows why discipline is so important when it comes to investing and reinforces the importance of our message from February 24th – avoid making portfolio changes based on average intra-year volatility. It is imperative to stay invested and not make portfolio decisions based on the “exogenous variable du jour” (in this case the Ukrainian invasion).

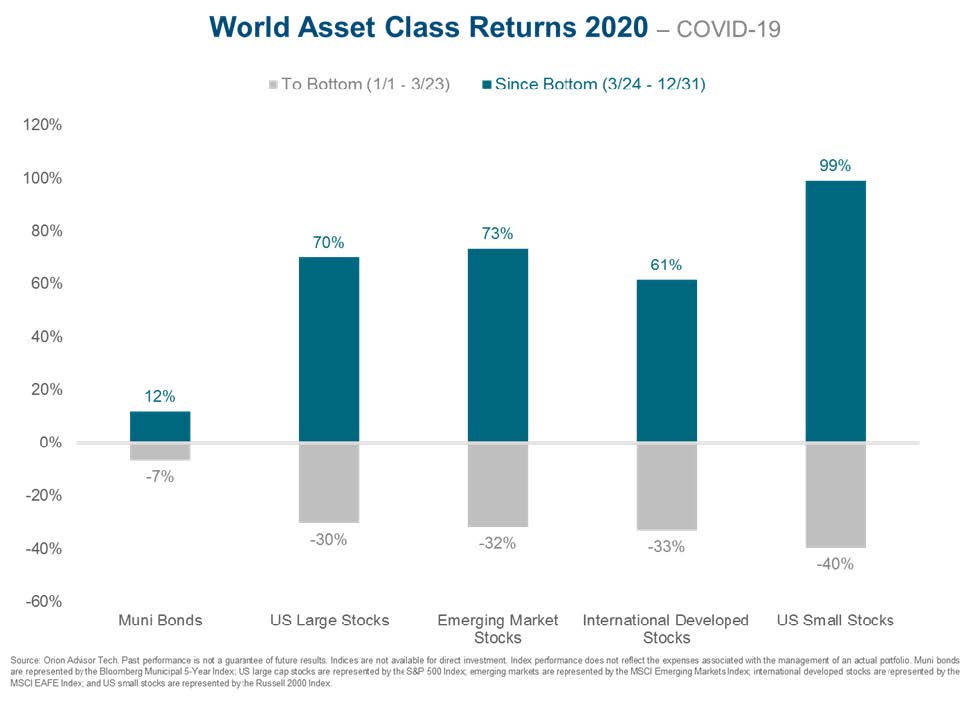

History tends to repeat itself, or at least rhyme. In 2020, the global markets experienced a sharp decline due to fears associated with COVID-19, bottoming on March 23rd, 2020. Following this sharp decline, the markets roared back with many asset classes finishing the year positive. Disciplined investors experienced positive returns in 2020. The below graph represents this – the grey bars show the return of their respective asset class from the beginning of the year through March 23rd (the 2020 bottom). The blue bars show the return of each asset class from March 24th through the end of the year.

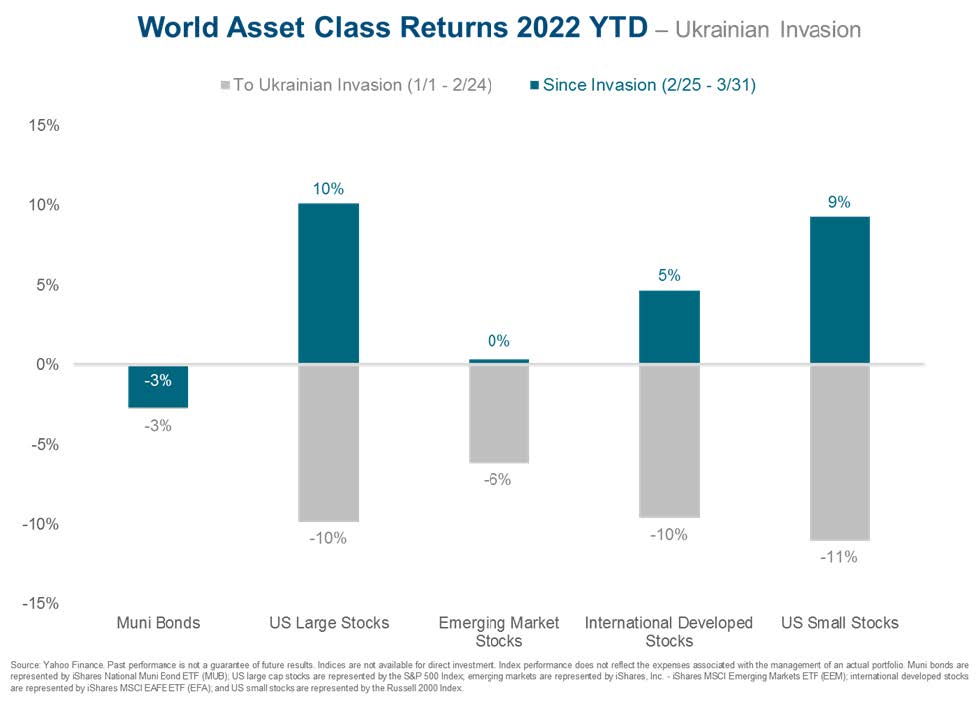

In 2022, we are experiencing a similar market reaction. The markets started the year down due to fears of inflation, rising interest rates, followed by the Russia/Ukraine conflict. As previously mentioned, the S&P 500’s low for the year was on February 24th, the morning of the Ukrainian invasion. Since then, most asset classes have experienced positive returns. The below graph shows this:

Moving Forward:

We are witnessing a tectonic shift in the world’s geopolitical order, engineered by Russia’s tragic war on Ukraine. Commodity prices, specifically oil, have surged. The offshoring of manufacturing to Asia has run afoul as severe supply chain issues remain. There is a growing realism that China cannot be relied on to be a rational actor. On top of all this, we find ourselves in the throes of the most severe inflation outbreak in nearly 40 years.

No one can predict how these problems will resolve themselves. We cannot possibly forecast how the capital markets will respond to their progression or resolution. We are in a fog of uncertainty and unknowing.

What we do know, and have great clarity on, is that current events are irrelevant to the investment policy of the long-term investor, especially the long-term equity investor. Continuing to practice rationality in the midst of uncertainty is the essence of the successful long-term investor. This means basing our investment policy on a personal financial plan – as distinctly opposed to an opinion of the economy or markets. Our advice continues to be the same – start with a plan, understand why you are investing, diversify for safety, and then stay invested and stay disciplined. During this volatility, we will continue to add value to your portfolio by tax-loss harvesting and rebalancing.

None of this is to make light of what has happened in Ukraine or any negative returns in your portfolio. Our hearts go out to all of those affected by this awful war. The media, in their attempt to sell newspapers and garner clicks online, tend to focus on the most disturbing and troubling events and outcomes. It is best to not let this affect your investment portfolio decision-making. We pray for a swift and peaceful resolution to the conflict. As always, please do not hesitate to reach out with any questions or concerns.

Best regards,

P.S. While I signed this memo, I want to credit our newest colleague, Brendan McEwan, with much of its content and graphical design. You’ll hear more about Brendan in the near future, he is a talented addition to our firm.

Alexander Lazieh, better known as Zander, joined RZH Advisors in August 2021 as a trader. He works in tandem with Carl and Spencer to supervise and manage our investment portfolios. He has a terrific work ethic and makes it his goal to learn something new each day. Zander takes great pride in his work and approaches each day dedicated to making our client experience as good as it can be.

Prior to joining RZH, Zander worked for a similar investment advisor in Rhode Island. He has significant experience monitoring, re-balancing, and trading client accounts. Don’t let his quiet personality fool you, he is quite the student of the markets and is extremely detail oriented.

Zander grew up in North Providence, RI and loves to spend time outdoors hiking, fishing and hunting. In his spare time, he is also an avid reader, mostly investment or economic related of course. He earned his bachelor’s degree from Salve Regina University.

Please join us in welcoming Zander to the RZH team!

Less than 40 days ago I delivered our 2021 Year End Letter which included the following:

“In general, consensus for the coming year is that (a) the lethality of the virus continues to wane, (b) the world economy continues to reopen and supply chain issues clear (c)corporate earnings continue to advance, (d) the Federal Reserve begins draining excess liquidity from the banking system, (e) inflation subsides somewhat, and (f) barring some other exogenous variable – which we can never really do – equity values continue to advance, though at something less (and probably a lot less) than the blazing pace at which they’ve been soaring since the market trough of March 2020. Please don’t mistake this for a forecast on my part. This is merely market consensus of outcomes that seem more likely than not. I’m fully prepared for any or all of the above points to be wrong; if and when they are, my recommendations to you will be unaffected, since our investment policy is driven entirely by the plan we’ve made, and not by current events.”

Russia/Ukraine is the exogenous variable du jour. The investment policy of a goal focused, plan-driven, long-term investor should be unaffected by it.

Before rallying to close today above 4,285 (actually rising 1.4% today) the S+P 500 fell to about 4,114 – down about 14% from its January 3rd high. Does this number ring a bell? 14% is the average intra-year drawdown for the S+P 500 over the last 40 years. As your financial advisor and steward, we do not suggest changes based on average market volatility. I know this does not feel “average” but so far it has been, at least in terms of market reaction.

What we have been doing over the last few weeks is being proactive in this environment: adding value by tax-loss harvesting, rebalancing strategies, shortening bond duration, and increasing the market capitalization of our stock holdings.

Carl’s obligatory statistic on this: looking back through the history of similar geopolitical events the average duration of market decline is three weeks – followed by three weeks of recovery.

All of this aside, the news of the day is very disturbing and unsettling. The media is extrapolating today’s events to unthinkable outcomes. This is normally the case with unforeseen geopolitical conflict. All of us at RZH are here for you and ready to speak about your planning and portfolio. Please do not hesitate to reach out.

Based on returns, 2021 appeared to be a good year for investors. US large company stocks rose 28% and international developed market stocks gained 11%. However, emerging market stocks fell 2% and the world’s second-largest economy, China, saw its stock market fall 5%. Taxable bonds declined slightly and municipal bonds rose slightly. And, surprisingly, even with rising inflation, gold fell 4%. Diversification did not help returns, 2021 was all about US large company stocks.

For a comprehensive review of the capital markets in 2021 CLICK HERE

Emotionally however, 2021 was a difficult year for investors – beginning with a contested presidential election, followed by “meme” stock mania, supply chain disruptions, the Delta and Omicron variants, labor shortages, historically high inflation, rising interest rates and political drama over the Build Back Better legislation. Despite all these worries, the US stock market was extremely resilient and barely declined by more than 5% at any point during the year. The market was positive in 9 of 12 months with two of those monthly declines being roughly 1%. Believe it or not, 2021 was one of the lowest volatility years in recent history for the US stock market. I do not expect the same for 2022.

However, it would be counterproductive to look at these past 12 months in isolation. In 2020 the world responded to the onset of the pandemic essentially by shutting down the global economy to prevent the spread of Covid. In this country, we experienced the fastest economic recession ever and a 35% decline in the S&P 500 in just 33 days.

Congress and the Federal Reserve responded with a wave of fiscal and monetary stimulus which was and remains without historical precedent. This point cannot be overstressed: we are in the midst of a fiscal and monetary experiment that has no direct precedent. This renders all economic forecasting – and all investment policy based on such forecasts – quite speculative.

If 2020 was the year of the virus, 2021 was the year of the vaccines. Hopefully, 2022 will be the year of a return to “normalcy.”

In general, consensus for the coming year is that (a) the lethality of the virus continues to wane, (b) the world economy continues to reopen and supply chain issues clear (c) corporate earnings continue to advance, (d) the Federal Reserve begins draining excess liquidity from the banking system, (e) inflation

subsides somewhat, and (f) barring some other exogenous variable – which we can never really do – equity values continue to advance, though at something less (and probably a lot less) than the blazing pace at which they’ve been soaring since the market trough of March 2020.

Please don’t mistake this for a forecast on my part. This is merely market consensus of outcomes that seem more likely than not. I’m fully prepared for any or all of the above points to be wrong; if and when they are, my recommendations to you will be unaffected, since our investment policy is driven entirely by the plan we’ve made, and not by current events.

With that said, I’ll offer a personal observation: these have undoubtedly been the two most shocking and nerve-wracking years for investors since the Global Financial Crisis of 2008-09 – first the outbreak of the pandemic, next the bitterly partisan election, then the pandemic’s second major wave, and most recently a 40-year inflation spike. You might not be human if you haven’t experienced serious headline fatigue at some point. I know I have.

But like 2008-09, what came to matter most was not what the economy or the markets did, but what the investor themselves did. If the investor fled the equity market during either crisis – their investment results seem unlikely ever to have recovered. If on the other hand they kept acting on a long-term plan rather than reacting to current events, positive outcomes followed. It has always been this way and I expect it always will be.

As we look ahead to 2022 there remains more than enough uncertainty to go around: inflation, the Fed’s response to inflation, rising interest rates, Covid, mid-term elections, a concentrated stock market, geopolitical unease in Russia and China…the list (always) goes on and on. So, might the coming year be a

lackluster or even declining year for the stock market as is usually the case when the Federal Reserve tightens monetary policy?

CARL BEING CARL…Yes, this is certainly possible. Now, how do you and I – as long-term, goal-focused investors – make investment policy out of that possibility? My answer: we don’t, because one can’t. Volatility and uncertainty are inherent components of investing and we know that attempts to predict

and avoid pullbacks are generally futile. Our strategy, as 2022 dawns, is entirely driven by the steadfast principles of the RZH Investment Philosophy (see below). I have no doubt that equities will probably experience increased volatility, but we have a plan for this. We act on your plan and do not react to the markets or current events. This was the most effective approach to the uncertainty of 2020 and 2021, and I believe it is the most sensible approach going forward.

We look forward to discussing this further with you in our annual review session. Until then, all of us at RZH thank you again for being our clients. It is a privilege to serve you.

Best regards,

General Principles of the RZH Investment Philosophy

It is goal-focused and planning-driven, as sharply distinguished from an approach that is market-focused and current-events-driven. Long-term investment success comes from continuously acting on a plan. Investment failure often results from continually reacting to current events in the economy and the markets.

History has shown that the economy cannot be consistently forecast, nor the markets consistently timed. You and RZH are long-term investors, working steadily toward the achievement of your most cherished lifetime goals. We make no attempt to forecast, much less time, the equity markets; these efforts have a historically very low probability of success.

Since 1980, the average annual price decline from a peak to a trough in the S&P 500 exceeded 14%. One year in five, the decline has averaged at least 30%. On two occasions (in 2000-02 and 2007-09), the Index has actually declined 50%. Yet the S&P 500 came into 1980 at 106 and went out of 2021 at 4,766. Over those 42 years, its average annual compound rate of total return (with dividends reinvested) was more than 12%.

Since we accept that the stock market cannot be consistently timed by us or anyone, we believe that the only way to be sure of capturing the full premium return of stocks is to ride out their frequent but ultimately temporary declines.

Factors that add a significant amount of value to an investment plan are: keeping costs low, being diversified, focusing on tax efficiency, staying relatively liquid, and matching asset allocation and investments with objectives.

Our essential principles of goal-focused portfolio management remain unchanged:

The performance of a portfolio relative to a market benchmark is largely irrelevant to long-term financial success.

The only benchmark we should care about is the one that indicates whether we are on track to accomplish your financial goals.

Risk should be measured as the probability that we won’t achieve our goals.

Investing should have the exclusive goal of minimizing the risk of not achieving your goals.